Diving into the world of algorithmic trading can be exciting and overwhelming at the same time. There are so many different approaches to developing your own algorithmic trading strategies. Especially for newcomers, this can be very intimidating.

To help gain a much deeper understanding of the world of quantitative trading, I want to give you an overview of all the different algorithmic trading strategies that exist. Besides improving your understanding, this should also help you decide what kind of algorithmic trading strategy you want to learn more about. No matter, your risk tolerance, preferred time frame, and favorite asset class, there is a right strategy that is right for you.

Here is a list of the top 6 algorithmic trading strategies that I will break down in this article. Note that some of these strategies can and are also used by discretionary traders.

- Mean Reversion

- Statistical Arbitrage

- Momentum

- Trend Following

- Market Making & Order Execution

- Sentiment Analysis

If you are completely new to algorithmic trading, I recommend first checking out my introduction to algorithmic trading.

Algorithmic Trading Strategies Video Breakdown

Check out the following video lesson in which I break down all the different types of algorithmic trading strategies.

Mean Reversion

Let’s start with one of the most commonly used algorithmic trading startegies, namely mean reversion strategies.

Mean reversion strategies are based on the assumption that stock prices will revert to their average price over time. Regression to the mean is a widespread phenomenon that can be found in many fields besides trading. For instance, if you go out for a walk and see a very tall person, chances are high that the next person you see is shorter and thus closer to the mean.

In mean reversion strategies, we try to apply this concept to stock prices. For example, if the market has a huge rally in one week, we might bet on that the market won’t rise as much next month. In other words, we expect next month’s move to be closer to the average.

The simplest form of mean reversion would be to use one or multiple moving averages of the stock’s price and trade around the discrepancy between this average and the stock’s price. This obviously is a very simple mean reversion strategy and likely won’t result in a desirable outcome.

Therefore, a popular alternative to just looking at one security is to look at multiple different securities and their correlation. This type of mean reversion strategy is known as pairs trading. Let me give you a specific example to clarify this:

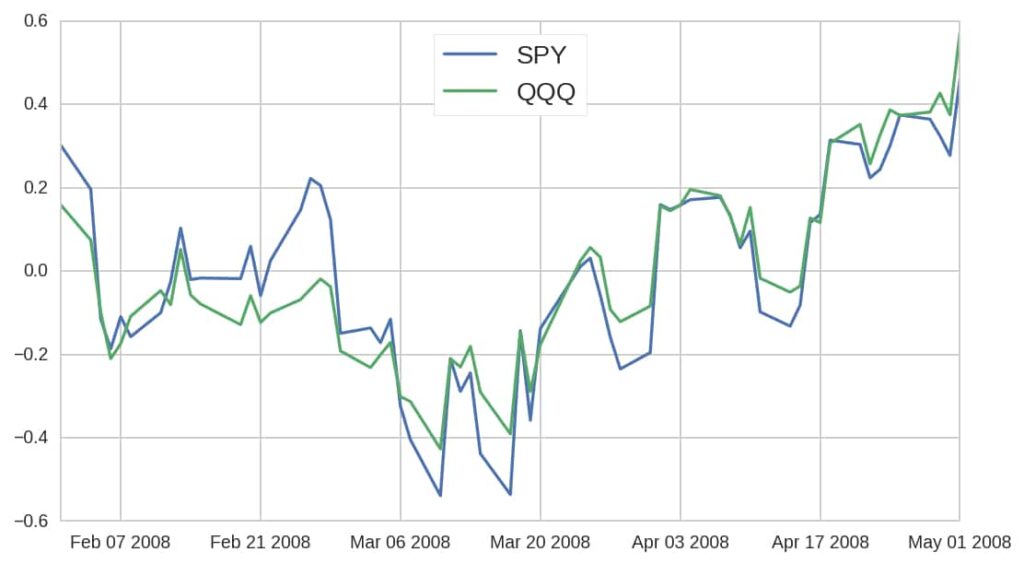

The following graph shows the normalized price moves of the exchange-traded funds SPY and QQQ at the beginning of 2008. As you can see, these two securities are closely correlated. This means they often move in sync with each other.

When SPY moves up, QQQ tends to do the same and vice versa. But since the two are still individual securities they do sometimes disperse from each other. Each of these dispersions is an opportunity since they mostly return to their normal state relatively fast.

For instance, at the end of February 2008, SPY had a relatively big rally whereas QQQ’s price didn’t change by much. This creates the opportunity to sell SPY and simultaneously buy the same amount of QQQ. Shortly after, their prices should move closer to each other again and you can then close the positions for a profit.

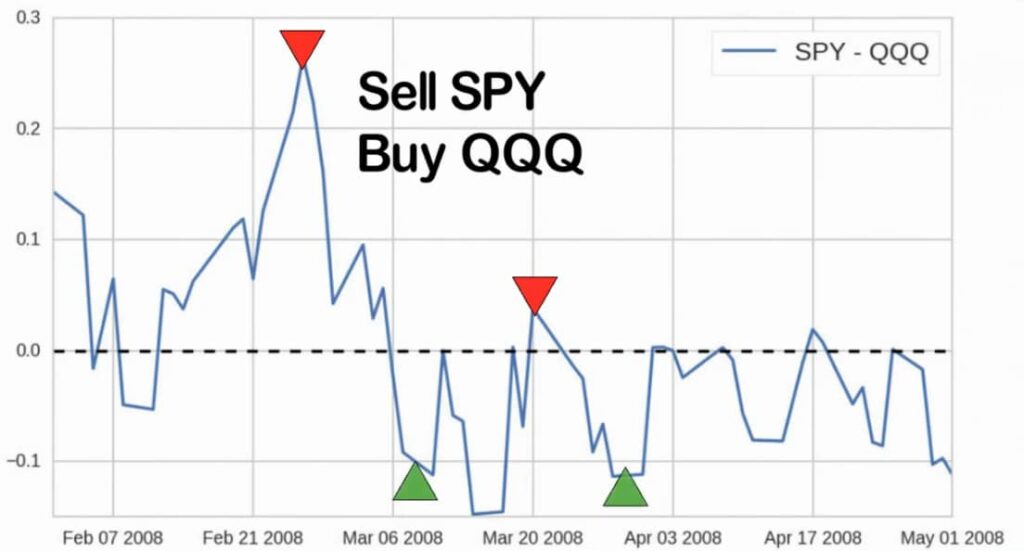

This second chart graphs the difference between SPY’s and QQQ’s normalized price during this same period. As you can see, during this time, the difference always drops back down to zero after some time. Therefore, it can be profitable to sell SPY and buy QQQ if this chart goes high enough and do the opposite if it drops down far enough. Every time it reaches zero, you can close the positions for a profit.

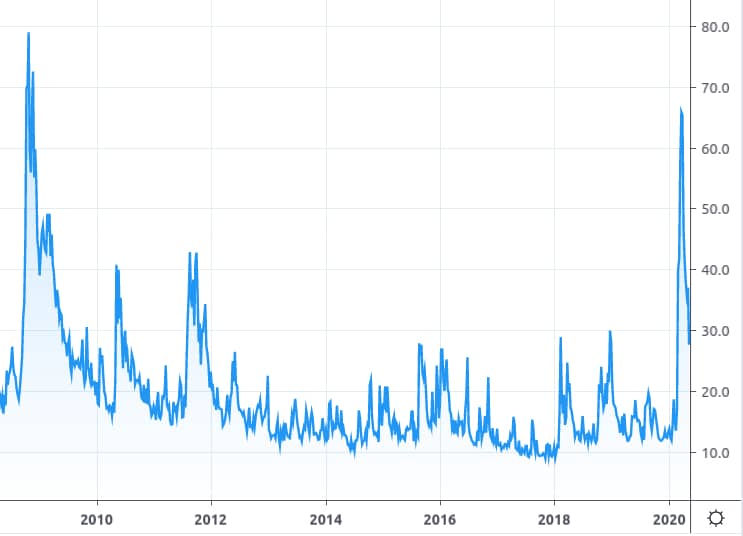

Besides pairs trading, another popular mean reversion strategy is selling options when implied volatility is high. Implied volatility can be thought of as the expected future volatility extracted from an option’s price. So when investors expect prices to be extra volatile, they tend to buy more options which will increase option’s prices and thus implied volatility as well. One of the most well-known tickers that tracks the implied volatility of the S&P500 options is the CBOE Volatility Index or just VIX.

The average price of VIX is slightly below 20, but once in a while, VIX’s price spikes up. Each of these spikes represents a huge expansion in options’ prices. By selling options, you can profit from the contraction after each of these price spikes since implied volatility and thus options prices tend to drop back down to their normal state relatively fast.

To learn more about selling options, make sure to check out my free options trading education.

Besides the just mentioned mean reversion strategies, there are many other types of mean reversion strategies. But I hope these examples gave you a good overview of what mean reversion strategies are and how they work.

Statistical Arbitrage

Statistical Arbitrage or just Stat Arb, in short, is a different type of algorithmic trading strategy that also uses mean reversion a lot. It takes advantage of pricing inefficiencies and employs statistical and mathematical models to identify opportunities. It can be thought of as a more advanced version of pairs trading. Instead of looking at a single pair of securities, statistical arbitrage strategies usually use dozens if not hundreds of different securities and look at their correlations. Typically, the time frame of statistical arbitrage strategies is very short and can be as low as a few seconds since pricing inefficiencies usually don’t last very long. Due to its complexity, statistical arbitrage is much more popular amongst professional trading firms such as hedge funds than among retail traders.

Momentum

Next up, let’s take a look at a different type of algorithmic trading strategy, namely momentum strategies. Momentum strategies are pretty much the exact opposite of mean reversion strategies. Instead of betting on prices returning to some state, momentum strategies try to profit from a continuation of a certain move. The underlying assumption for such strategies is that price moves can hold their momentum for an extended period of time. Let’s go over a few examples to clarify this.

A classic momentum strategy is the so-called ‘gap and go’ strategy. This is a strategy that looks for overnight gappers and bets on a continuation of this move. For instance, if stock XYZ gaps up by 2% overnight, this strategy might seek to establish a shorter-term long position in XYZ. Note that this is the exact opposite of what a mean reversion strategy would do.

Another popular momentum strategy is an earnings or other news event fueled price move continuation bet. Since a major news event surrounding a company can have a lasting impact on its stock’s price, you could try to be early enough and bet on a continuation of this price move. Furthermore, you can also couple this news event with an overnight gap to create a slightly more advanced strategy.

Other momentum strategies include sector momentum, breakout, and breakdown strategies among others. Typically momentum strategies focus on short term setups.

Trend Following

Trend following strategies are the longer-term adaptation of momentum strategies and to be honest, they are rather self-explanatory. They try to identify price trends and take advantage of them by following the found trend. Usually, these are longer-term trends, but they can also be mid to short term. The exact definition of a trend depends on the chosen implementation of a trend following algorithm.

Market Making & Order Execution

Another common type of algorithmic trading strategy is a market-making or execution based strategy. This type of strategy can’t really be deployed by retail traders, but that doesn’t make it entirely irrelevant which is why I briefly want to cover it. When big institutions such as banks or funds want to open or close a position, they can’t just buy or sell it on the open market as you or I would. This is because their position sizes are so huge that if they were to sell or buy in one go, they would push the entire market in one direction. Besides exposing their trade action to everyone else, this would also lead to unfavorable entry and exit prices for them. This is an especially big problem in illiquid markets. So what institutions do instead is, open or close their positions in many different smaller orders.

Sadly, dividing your order into may small orders doesn’t completely solve this problem since it still creates a lot of pressure in one direction of the underlying. That’s why they use execution based algorithms that try to find the best possible places to send out more orders without affecting the price too much.

Identifying that a big institution is currently using such an execution based algorithm allows you to trade around this algorithm. That’s why market makers often use so-called sniffing algorithms that try to find and profit from big order executions through these algorithms.

High-frequency trading strategies usually fall into this category of algorithmic trading strategies.

Sentiment Analysis

Last but not least, let’s take a look at sentiment analysis algos. Sentiment analysis algorithms look at people’s current opinions and attitudes toward a given security and generate a market assumption around the result. Usually, these algorithms look at millions of data points to best possible evaluate the current sentiment. Typical sources for this data are news networks, social media such as twitter, google searches, and more. A sentiment analysis algorithm might, for example, go through thousands of tweets that include a mention of a certain company and analyze whether these mentions are mostly positive or negative.

If, for instance, Apple just released a new phone and everyone on the internet is talking negatively about it, a sentiment analysis algo might generate a sell signal.

If, on the other hand, the general consensus is that the new phone is amazing and enough people express this opinion online, the algorithm might suggest a bullish position.

It can, however, be hard to accurately measure sentiment due to its obvious subjectivity. But if sophisticated enough models are used, you can certainly gain insights into consumer sentiment. Nevertheless, this type of algorithm is best used in conjunction with others.

Conclusion

In general, all of these strategies can be combined with others to create more complex and potentially more reliable strategies. Furthermore, none of these strategies is the holy grail trading strategy. All have their differences and thus their strengths and weaknesses. Most of these strategies can be customized so that they are best suited for your and your preferences.

Note that this article just covered general trading strategies. These are abstract ideas that can be used to gain inspiration. An actual trading strategy should be implemented much more concretely with clearly defined trading rules including your risk and profit potential, the time frame, asset class, capital allocation, and more.

Regardless of what strategy you want to use, it is very important to implement solid risk management practices. Otherwise, you are just sitting on a ticking time bomb.

With that being said, I hope this post gave you a good overview of what kind of algorithmic trading strategies exist. Let me know which of these strategies is your favorite in the comment section below!

Thank you for an excellent overview of the top 6 algorithmic trading strategies. They would indeed be good reference strategies in navigating the complex world of trading. Fully agree with you that one has to discern the pros and cons of each strategy, assess them against one’s decision criteria and choose one or a combination that would best meet his trading objectives taking into account your personal level of risk aversion.

Great and insightful article. Thanks again!

Thanks for the comment. I am glad you liked it.

Thank you for your post. It is informational and educational. There are so many strategies in stock tradings and it is important to pick the best one to exercise one’s trading.

I like the trending strategy. The critical step for a successful trending trader is to identify the trend of a stock. Depending on your trading approaches, you need to have clear trend definition of the stock. If you are short term stock trader or day trader, you definitely need to have grasp of the short term trend of the stocks you are going to trade. If you are long term stock trader, you need to have knowledge of long term trend of the stocks you are going to trade. In any cases, trend is friend, never against the trend, instead follow the trend.

Hi Anthony,

Thanks for sharing your insights. I certainly agree that it can be very helpful to consider different time frames when looking at an asset’s trend.

Hello Louis! This an amazing review we got here.Thank you for an excellent overview of the top 6 algorithmic trading strategies.though is my first time hearing about it but with the look of it and little I read about it I got an amazing information form it which we help me out in all areas trade am ik into an really greatful.

Thank louis for sharing this with me

Thanks for the comment. If you are completely new to algorithmic trading, you could check out my introduction to algorithmic trading.

Hello Louis! this review is super helpful for me. A close friend of mine who’s a pro in algorithmic trade tried teaching me this the statistic strategy of the trade but I gave up the class because it was super difficult for me to understand.

I just hope going through your introduction to algorithmic trading will help me get the rudiments of this trade. Thanks for sharing.

Wow! Thank you very much for sharing this with me, I have already save this post so i can go over again. Before then, I think i need to go through your previous review on the basic of this trade as I got confused at the part you were talking about statistical strategy.

Thanks for sharing.

Quite an impressive article on Algorithmic trading strategies, its important you know that Algorithmic trading (also called automated trading, black-box trading, or algo-trading) uses a computer program that follows a defined set of instructions (an algorithm) to place a trade. The trade, in theory, can generate profits at a speed and frequency that is impossible for a human trader.

Hope you get to understand the important of Algorithmic trading before you venture into it and I hope these Six strategies helps and I look to se3 more from you.,.

Thanks for sharing your insights.

Wow! This is an awesome article.

These are nice algorithm trading strategies. However, the Statistical Arbitrage caught my interest because it takes advantage of inefficiencies through statistical models unlike the mean reversion and sentimental analysis.

If such an algorithm finds an inefficiency is that a risk free profit opportunity or is there still some risk of losing money?

Thanks for the help.

There are some algorithmic strategies that look for true arbitrage opportunities that exist due to actual incorrect pricing. If such an inefficiency is found, it is more or less a risk free profit. However, since these inefficiencies are very scarce, statistical arbitrage strategies focus more on historical/statistical correlations and trends that have a very high likelihood of continuing. Finding and trading around inefficiencies in this area isn’t exactly risk free, but it tends to be quite low risk. But at the end of the day, the risk of a given strategy comes down to its concrete implementation and the models that it is based on.

Greetings and Regards

Thank you very much from the publication of this article

There was a lot of good and useful content.

I was very interested in starting the Arbitrage and Market Making section.

I am very interested in tried with robot trading. ((I also need a very strong and sure strategy)).

If you have things in this case and you can help me get so happy to help.

Best Regards