Hedging your investments is one of the best ways to systematically decrease your risk and thereby increase your risk to return ratio. But when hedging your portfolio, there are certain things you have to look out for. In this article, you will learn whether or not you should hedge your portfolio and two of the most effective approaches to hedging with options.

Why Hedge

A hedge is a position that was opened to offset risk. This can be both upside or downside risk, but in this article, we will focus on downside risk since the majority of investors don’t have negative upward exposure.

Before we get into how to create the most effective hedge, let’s first take a look at why you should or should not have a hedge in the first place. The first and most obvious benefit of hedging your portfolio is that it reduces risk. A hedge protects your position(s) from black swan events such as market crashes or other sharp drops. Depending on the implementation of your hedging strategy, it might also protect you against other minor price declines. In general, an effective hedge will reduce the (downward) volatility of your position(s).

Sounds great, right? So why not always have a hedge?

The biggest downside of a hedge is that it costs money. A hedge will protect you against bearish price action, but if prices don’t drop, there is nothing to be protected from. In this case the costs associated with the hedge will eat into your profit potential. Therefore, hedged portfolios will typically underperform unhedged portfolios in sideways and bull markets.

Nevertheless, hedges can be a great way to protect your trading livelihood in uncertain times. Furthermore, an abundance of trading models (including the Black Scholes options pricing model) assume that stock prices are normally distributed. This leads to a systematic underestimation of the likelihood of big price drops. This risk is called fat tail risk or kurtosis risk and one of the only ways to reduce this kind of risk is by hedging your investments. To learn more about this topic, check out my post on the probability distribution of stocks.

In addition to protecting you from large price drops, a hedge will always guarantee you peace of mind since you no longer have to worry about any upcoming disasters. In this sense, a hedge can be thought of as an insurance product against price crashes. From the view of the customer, most insurance products have a negative expected return. But most people are willing to pay a premium for their peace of mind.

Here is a small table that sums up some of the advantages and disadvantages of hedging your positions:

| Advantages | Disadvantages |

| Reduces Risk & Volatility | Hedge costs can reduce performance in bull markets |

| Peace of Mind | It takes time to implement hedging strategies |

The Best Hedging Strategies

Now that we covered the pros and cons of hedging, let’s take a look at a few concrete hedging strategies that you can use for your portfolio.

Protective Put Hedge

This is the most basic and most commonly used hedging strategy. Put options allow you to sell the underlying asset at a predetermined price (also known as the strike price). Buying a put is a great way to limit the downside risk of your position.

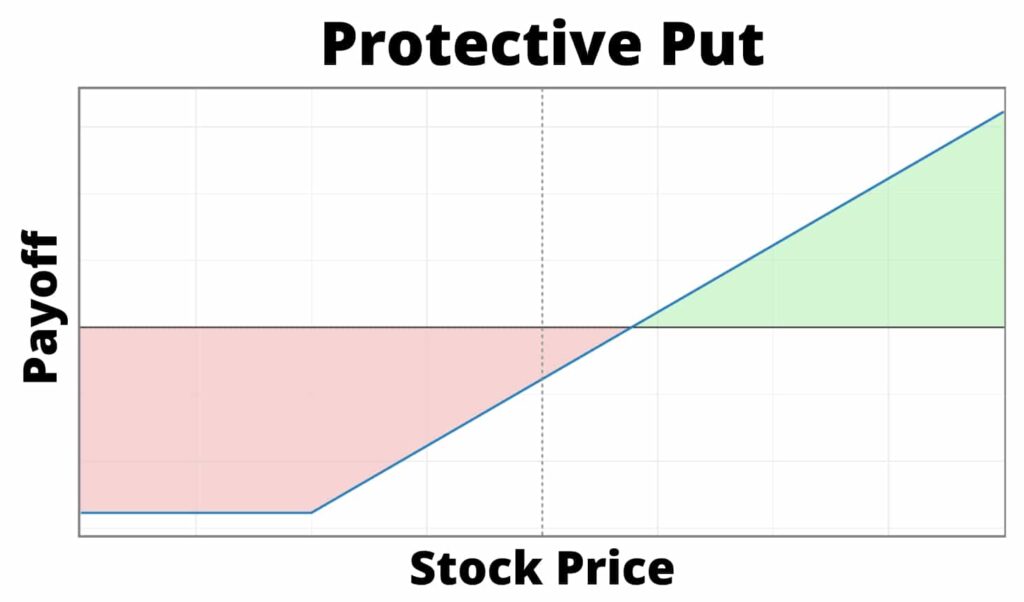

This chart shows the payoff profile of a protective put. As you can see, the protective put does not limit your profit potential. But in contrast to a normal stock position, a protective put caps your loss at a certain point. This means as soon as the stock price surpasses the strike price of the put option, you hit the max loss point (regardless of how much lower the price continues to drop).

Since you are paying a premium to buy this put option, your overall breakeven point is moved upwards. The amount by which the breakeven point is increased depends on the price of the option.

Setup

One of the best things about a protective put is its simplicity. All you have to do is buy 1 put option for every 100 shares that you own. So if you have a position of 300 shares in XYZ, you would have to buy 3 put options.

Sounds simple, right?

That’s because it is. The only caveat is choosing the right put option to buy. Typically, there are dozens of put options to choose from for every expiration date. So how do you choose the best possible put option to buy?

Choosing the right strike price very much depends on what kind of protection you want to buy. The higher the strike price, the more protection the position offers. But the put option will also be more expensive and thus move the breakeven point up more. A put option with a lower strike price will offer less protection, but it won’t move your breakeven point as much since it will be much cheaper.

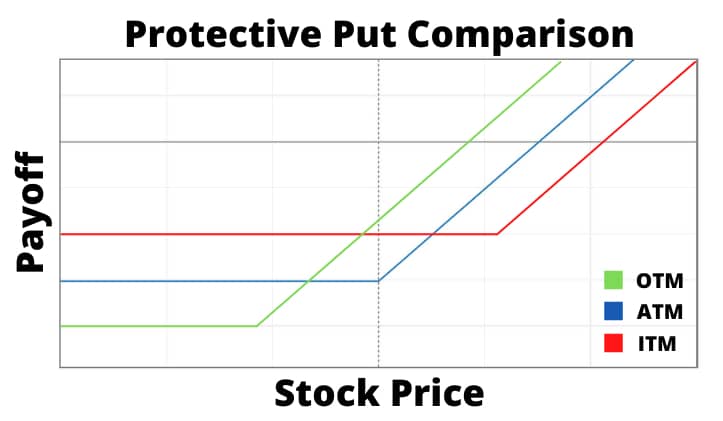

The following chart compares the payoff profile of an Out of The Money, At The Money, and In The Money protective put:

As you can see, choosing a strike price comes down to a tradeoff between protection and price of the put option. Generally, I recommend using OTM options over ITM or ATM options since they are by far the cheapest. Buying ITM options will just eat away any attempts at profit way too fast.

Besides choosing the right strike price, you also have to choose an expiration date. The naive choice of expiration is to simply buy a very long term option that expires in a year or two since this is the easiest solution. But in reality, this is probably one of the worst solutions. A good hedge should move up together with the underlying price. Otherwise, the underlying price can just move up and thereby constantly increase the downside risk.

That’s why it’s a good idea to buy a put option with a moderately long lifespan (1-2 months) and roll the long put up every time it reaches the expiration date. Using the option Greek Delta is a great way to make sure that you always buy the same level of protection. You could, for instance, buy a 30 delta put option with 60 days till expiration every 60 days.

A long put option has a positive Vega value which is the option Greek that measures the option’s sensitivity to changes in implied volatility. This means that the long put profits from increases in implied volatility. Typically, implied volatility increases when prices drop. So besides profiting from the falling prices, the protective put also profits from rising implied volatility.

On the flip side, a long put has a negative Theta which means that it loses some of its value every day due to time decay.

Pros & Cons of a Protective Put

| Pros | Cons |

| Easy to implement | Expensive |

| Offers guaranteed max loss | Requires you to roll often |

Performance

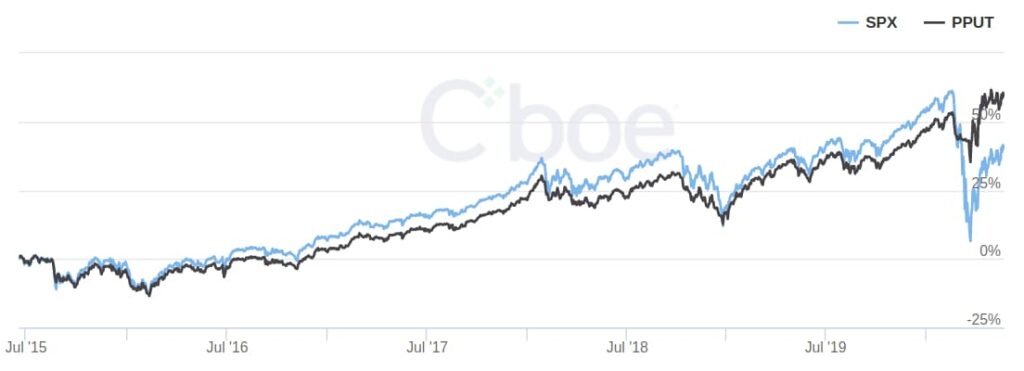

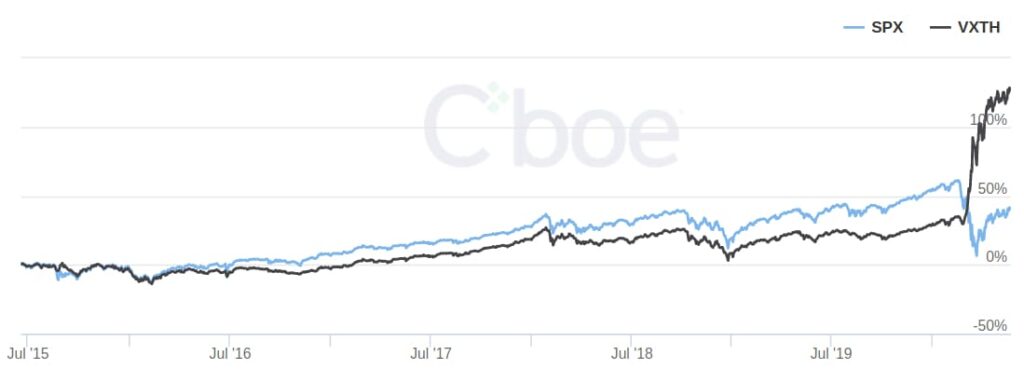

To get a rough gauge of the performance of a protective put portfolio, we’ll look at CBOE’s Put Protection Index (PPUT). This index tracks a theoretical portfolio that holds a long position that corresponds to the S&P500 Index as well as a protective put. The protective put is opened 5% Out of The Money with about 30 days till expiration.

The following chart compares the performance of this index to the S&P500 index (SPX).

As you can see, during the time leading up to 2020, the SPX index outperforms PPUT. But this changes with the March 2020 market crash. So over these 5 years the PPUT index has achieved a better total return with lower volatility.

Please note that this does not mean that a protective put hedged portfolio is better (or worse) than a portfolio without a hedge. This is only a comparison of these indexes during this specific time frame. During other time frames, the performance can vary dramatically. Especially, over the very long term, SPX tends to outperform PPUT. Also, note that there are many other ways to implement a protective put hedge strategy.

If you want to compare SPX and PPUT during other time frames, you can do so on the CBOE website or by entering these ticker symbols into a charting platform of your choice.

Variations

Before we move on to another hedging strategy, let’s cover a few variations to the standard protective put strategy. The first variation would be to buy a protective put for your entire portfolio instead of for individual positions. One way to do this is to find a major market index that is correlated to as many of your positions as possible and then buy a put option on this index. If you are trading equities, you could, for instance buy puts on SPY which is an ETF that tracks the S&P500 index. To make sure you buy the right amound, it is possible to use beta weighting. Check out my article on beta weighting to learn more about this.

Depending on the level of protection that you want, you could also set up an asymmetrical protective put. For instance, instead of buying 1 put for every 100 shares, you could buy 1 for every 150 shares. The advantage of this is that it is much cheaper. But on the flip side, this won’t offer you the same protection as a standard protective put.

VIX Call Hedge

Next up, let’s look at a great alternative to the protective put. Instead of buying a put option, you can also buy an inversely correlated security to hedge your position. If your position goes down, this inversely correlated security should go up and thus offset your losses. One of the best trading vehicles that is inversely correlated to an asset is its implied volatility.

Implied volatility is extracted from options prices and can be thought of as the expected future volatility. Typically, when prices drop, investors buy more options which pushes up options prices, and thus implied volatility increases as well. The great thing about implied volatility is that it mostly hovers around an average level and only really spikes if prices drop big.

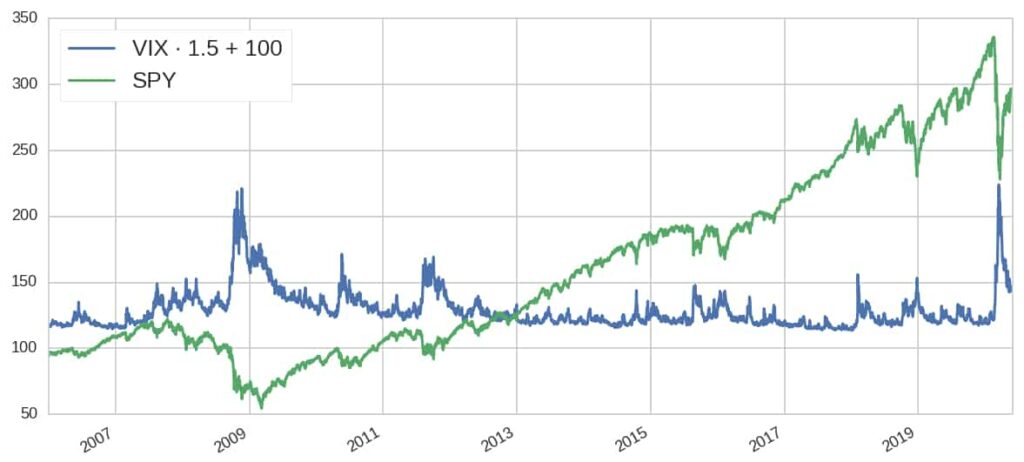

One of the most well known implied volatility indexes is the CBOE Volatility Index (VIX). The VIX tracks the implied volatility of the S&P500 options. The following chart compares VIX’s price chart to that of SPY:

It is clearly visible that VIX spikes when SPY drops. But VIX does not downtrend beyond a certain point when SPY uptrends. These two characteristics make buying VIX a great hedge. With that being said, it’s not possible to directly buy VIX since its just an index. But it is possible to open a long position through futures or call options. For this strategy, we’ll focus on buying call options since this is easier and requires less buying power than buying futures.

Setup

Just like the protective put, this strategy is quite easy to implement since all you have to do is buy a call option on an inversely correlated security such as VIX. Since VIX mostly hovers around its mean price, you won’t have to readjust your call option like you have to with the protective put. Nevertheless, you shouldn’t buy very long term VIX calls since they won’t offer the same sensitivity to potential VIX price spikes.

When choosing a strike price for the call option, you should consider the same criteria as for the protective put. ITM options will offer the best protection at the greatest expense, whereas far OTM options will offer the cheapest and least protection. Generally, a slightly OTM call option is the best choice due to its relatively low price.

Just like a protective put, a long call also has a negative Theta which means that it loses money from time decay. Options that are closer to expiration will have a higher rate of time decay than options with plenty of time left. But since call options have a defined max loss, they can’t lose more than a certain amount.

Generally speaking, VIX call options tend to be cheaper than SPY put options which makes this strategy even more attractive.

One disadvantage compared to the protective put, however, is that a VIX call hedge mainly protects against sharp price drops. Implied volatility does not spike nearly as much during slow downtrends compared to sharp declines. Therefore, the protection gained from buying VIX calls is best for sudden drops.

Performance

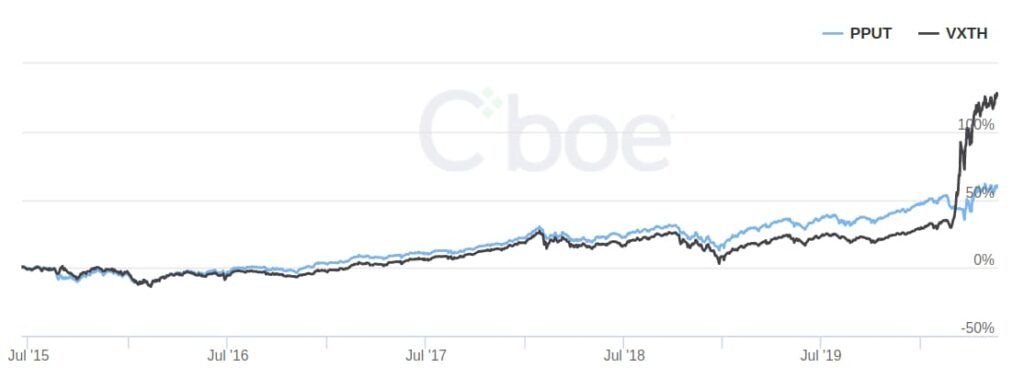

To get an idea of a VIX call hedge strategy’s performance, we’ll take a look at CBOE’s VIX Tail Hedge Index (VXTH). Similar to the PPUT index, the VXTH tracks a theoretical portfolio that buys and holds the S&P500 index as well as a dynamic amount of 30 delta VIX call options.

The following chart compares the performance of VXTH and SPX (S&P500 Index).

The VXTH chart looks very similar to the PPUT one with the main difference being the spike during the March 2020 crash. Since this was a very sharp price drop, VIX had a very fast and large spike which lead to an explosion in VIX call prices and thus a major profit for VIX call hedge buyers.

Here is a comparison between PPUT and VXTH during this same period:

As you can see, in bull markets and steady up trends, PPUT outperforms VXTH, but in a brutal crash PPUT stands no chance against VXTH.

Once again, I want to emphasize that this doesn’t mean that one strategy is better than the other. These indexes just give you a very rough idea about how one implementation of these strategies performed during a specific time frame. To get a better overview of these indexes, I recommend comparing them yourself.

Variations

Instead of using VIX call options, it is also possible to use some other inversely correlated security. Common alternatives include bonds & notes, certain equities, inverse ETFs… One advantage of using options is that they are very capital effective since they offer leverage. Furthermore, they have an asymmetrical payoff diagram which means that your max loss is limited whereas the profit potential isn’t capped. These two attributes are great for a hedge.

Besides buying inversely correlated securities, you can also decrease your unsystematic risk by diversifying your portfolio among multiple uncorrelated sectors and markets.

Hedged vs Unhedged Portfolio

Since you now know about two different options hedging strategies, you should have a much better understanding of the intricacies of hedging. Therefore, let us now discuss the question of whether you would be better off with or without a hedge.

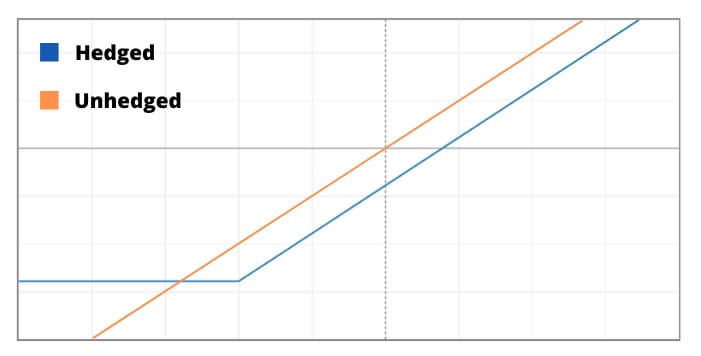

During a bull market, a hedge seems like an unnecessary expense, whereas a hedge can be a lifesaver during market crashes and bear markets. The following chart compares the payoff profile of a hedged vs unhedged long equity portfolio:

As you can see, the hedged portfolio (blue) only outperforms the unhedged portfolio in the case of a market drop. So the best-case scenario would be to have no hedge during bull markets and have a hedge in bear markets. Sadly, this isn’t possible since you never know when the next market crash will happen.

To answer the question of whether or not you should hedge your portfolio, you should consider and weigh the following metrics:

- Volatility: Hedged portfolios tend to have lower volatility than unhedged ones. If you want to keep portfolio volatility as low as possible, a hedge is a good way to do so.

- Maximum Drawdown: Since a hedge protects you from large price drops, the maximum drawdown of an unhedged portfolio typically is lower than the max drawdown of an unhedged portfolio. So a hedge can protect you against big drawdowns.

- Risk/Return Ratio: Due to the lower risk that a hedged portfolio offers, the Risk/Return ratio of a hedged portfolio often is better than that of an unhedged portfolio.

- Absolute Return & Time Frame: A hedge is an expense that can decrease your profit potential during bull markets. Therefore, over the long run unhedged buy & hold equity portfolios tend to outperform hedged buy & hold equity portfolios in regard to absolute return.

- Risk: Generally, a hedged portfolio is less risky than an unhedged portfolio. But the risk obviously depends on the market sector that you are trading. The riskier the sector, the more viable a hedge becomes.

Choosing whether you should or should not hedge your portfolio comes down to deciding how important these factors are for you and your investments.

If your goal is to simply buy and hold a well-diversified equities portfolio for the next decade or two and you don’t care that much about portfolio volatility, it might make more sense to not hedge your portfolio. But if you have a shorter-term approach and are active in a more risky sector of the market, you could stabilize your portfolio and avoid big losses by hedging.

With that being said, I hope this article gave you a good overview of what hedging possibilities options offer. Make sure to let me know if you have any comments or questions in the comment section below.

Great educational post and everyone who reads should bookmark as I have to allow time to digest the rich information you have provided here. I actually feel better about my portfolio after reading your post. It isn’t hedged but I tend to worry because I hear so much in the media of why it is important to hedge. For me, my investment portfolio doesn’t need to make me money now, I just need it in 15 years when I will retire. So, I need steady growth and your post in the short term has affirmed that I am doing the right thing. Thank you for a very informative and encouraging post.

Hi Lee,

Thanks for the comment. That’s great to hear.

This is quite interesting, especially in times like these, I was just going through a couple of articles of how the Covid19 is affecting the world’s economy, and how it will affect it even more. Do you think this strategy will be safer during this pandemic or it will also be hit hard?

Regards,

Juan

Hi Juan,

As you can see from the CBOE VXTH and PPUT indexes, these strategies have performed very well in 2020 so far.

I have always advocated that people make as much money as possible. I never gave much thought to the risks involved.

Thank you for this lesson on the need to always consider risk and reward. I now know the situations that require hedging, and those situations that do not require hedging.

Can the VIX Call Hedge be applied to every investment instrument? I would like to give it a try since it is the cheapest of both hedging strategies.

Thanks for the comment. I only recommend using VIX calls as a hedge for securities that are inversely correlated to VIX (calls). Most major equities fall into this category. But if you are trading low cap stocks, commodities, forex, bonds, or something else, you shouldn’t use VIX calls as a hedge. But the concept behind the VIX call hedge strategy can be applied in any market. You just have to find a suitable replacement for VIX in your sector.

I hope this helps. Definitely let me know if you have any follow up questions.

…….Thanks for bringing this at this time.

This is really encouraging, the COVID 19 situation should be an eye-opener that we need to be careful and make sure we plan ahead. Recent happening is already showing that the economy will be affected.

With people not having enough to spare do you still think this strategy is safer, even with the risk involved.

Hi Manuel,

Thanks for your comment. Hedging your investments is less risk and more conservative than not doing so. With that being said, there still is a significant amount of risk involved. This is the case regardless of your strategy. If you have nothing to spare and can’t afford to lose your money, you should not be investing it. Instead, save up until you have something to spare and then invest that if you are comfortable with the risks.

Hello dear, wow what wonderful content you have here, I must say I really fancy these page so much, I was actually doing some research online when I saw some articles on hedging with options. Most of them were very basic and didn’t cover the topic too in depth. But your article gave me all the information I wanted.

I’m glad to hear that.

I know that finding a good article does not come by so easily so i must commend your effort in creating such a beautiful website and writing an article to help others with useful information like this.The principle of using options to hedge against an existing portfolio is really quite simple, because it basically just involves buying or writing options to protect a position. For example, if you own stock in Company X, then buying puts based on Company X stock would be an effective hedge.

Thanks for the positive feedback. I really appreciate it.

Nice post! I’ve also heard about hedging using a put ratio spread (I think that’s what it’s called). You sell a pretty far OTM put, then buy 2 further out of the money. Or sell 3 and buy 5. The main thing is to buy more than you sell, and do so for a credit (or at least breakeven) if possible. If the market goes up, you make a little or at least don’t lose anything. If the market has a moderate loss, you might end up in a “valley of death” where you lose a defined amount. I guess this is the cost of insurance. If the market really tanks, you can make a lot of money. Have you heard of anything like this?

Also, Kirk at Options Alpha did a few videos about his take on the VIX hedge. From what I remember, you buy OTM VIX calls 120 days out (about 0.25% of your portfolio each month, or 3% annually). You buy them monthly, so you may get a “dollar cost averaging” effect of buying more when VIX is super low. You always own four which expire around 30, 60, 90 and 120 days out. Worst case you pay 3% for insurance. If the market crashes, you have protection and may profit. I believe he said it was slightly profitable during the period he tested it (around 2008-2018 IIRC). Unfortunately, I can’t find the video on Youtube any more. They still have a later video he did involving a VIX spread, but I like the pure call buying better.