The debit spread strategy is relative popular, easy and common for directional option trading. This defined risk vertical spread strategy is very similar to credit spreads. Differences are the risk profile and the more directional behavior of this spread. There are multiple different ways to set up debit spreads. I will be presenting the two most common ones.

Bull Call Debit Spread

Market Assumption:

When trading a Bull Call Debit Spread you obviously should have a bullish assumption. How bullish you should be depends on how far you go OTM. If you stay very close to the current price of the security, you can just be slightly bullish.

Setup:

- Buy 1 Call

- Sell 1 Call (higher strike)

This should result in a Debit (Pay to open)

Profit and Loss:

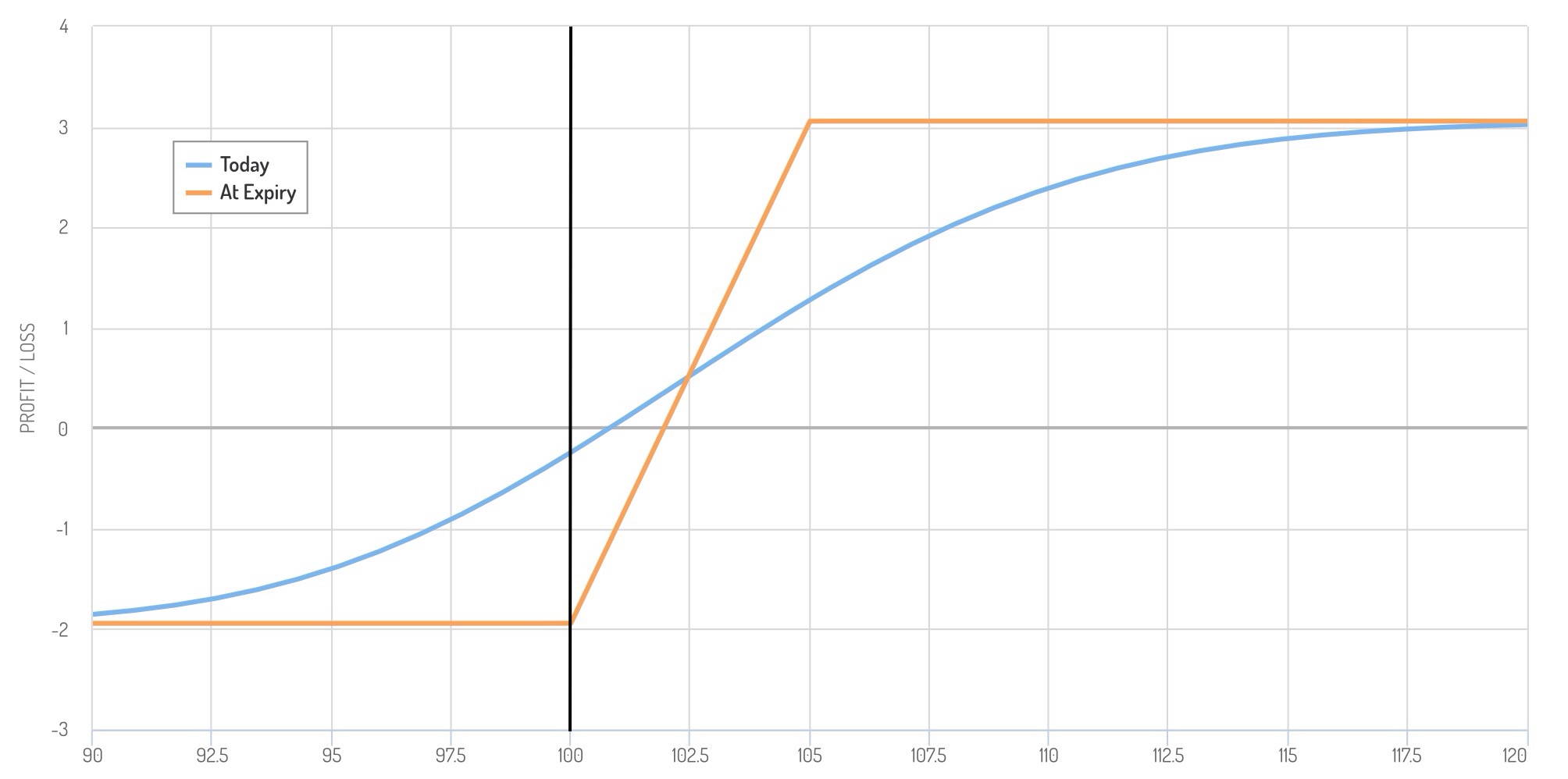

This can be a very profitable strategy. A Bull Call Debit Spread is a limited risk and limited profit strategy. The max profit is usually much higher than the max loss for debit spreads. Max profit is achieved when the price of the underlying is anywhere above the short strike. Max loss on the other hand occurs when the price is below the long strike. The break-even point is somewhere in between these strikes.

Maximum Profit: Strike of Short Call – Strike of Long Call (Width of Strikes) – Premium Paid – Commissions

Ex. 53 – 50 = 3 (3$ width of strikes) => 3$ *100 – 50$ (Premium Paid) – 5$ (Commission) = 245$ (max profit)

(a normal option contract controls 100 shares, therefore *100)

Maximum Loss: Premium Paid + Commissions

Ex. 50$ (Premium Paid) + 5$ (Commission) = 55$ (max loss)

Implied Volatility and Time Decay:

A Bull Call Debit Spread profits from a rise in implied volatility. This means it is best to use this strategy when IV is rather low (below IV rank 50).

Time Decay or the option Greek Theta works against this position and is therefore negative. Every day the long option loses some of its extrinsic value. The amount of value lost every day increases the closer you get to expiration.

Bear Put Debit Spread

Market Assumption:

As the name implies this is a bearish strategy and therefore your directional assumption should be bearish as well. The further you go OTM with this strategy the more bearish you should be.

Setup:

- Sell 1 Put

- Buy 1 Put (higher strike)

This should result in a debit (Pay to open)

Profit and Loss:

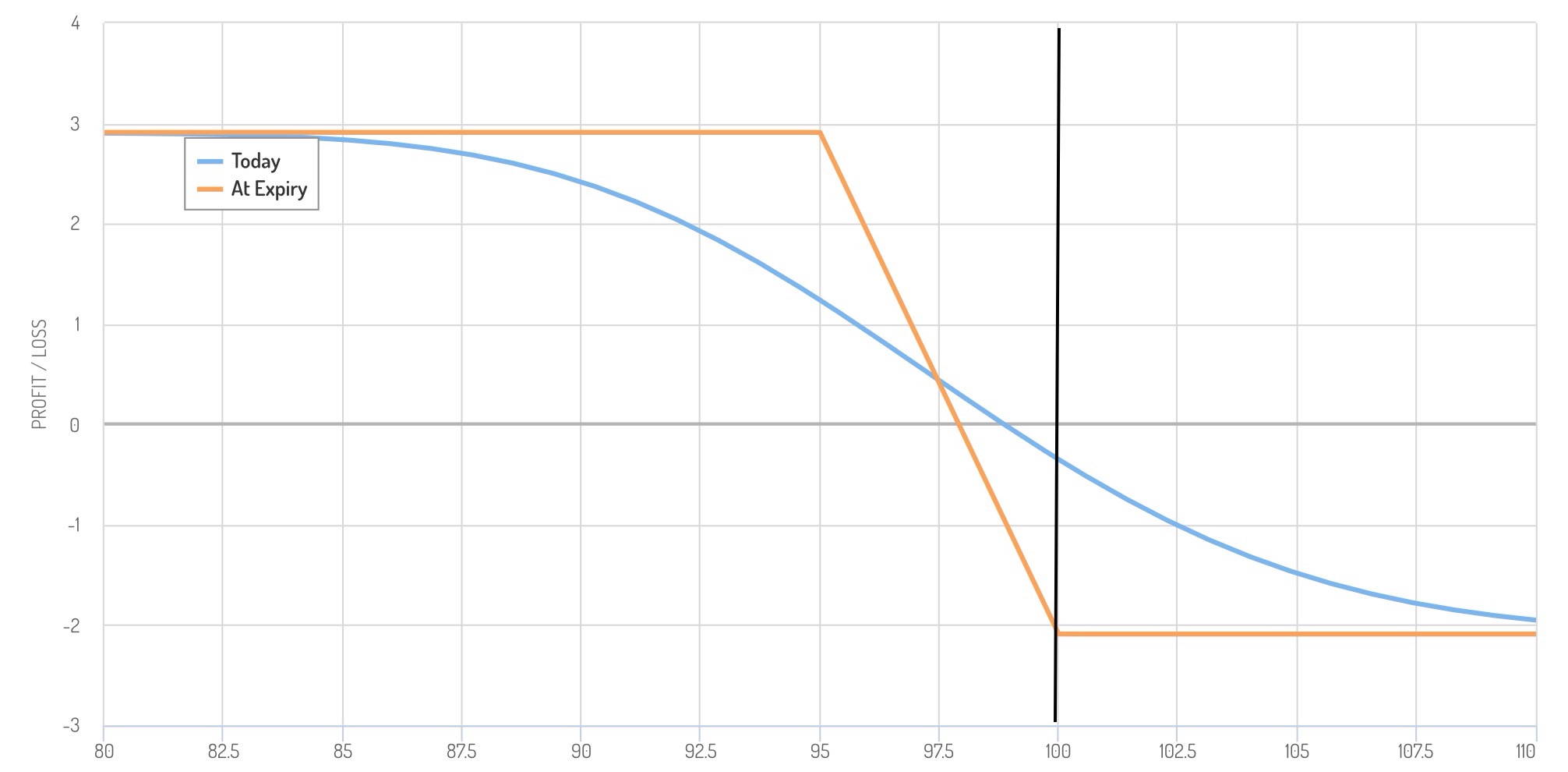

A Bear Put Debit Spread is a risk defined and limited profit strategy. The max profit achievable is greater than the max loss. The maximum profit is achieved when the price of the underlying is below the short option strike. The max loss happens when the price is above the long strike. The break-even point is between these two strikes.

Maximum Profit: Strike of Long Put – Strike of Short Put – Premium Paid – Commissions

Ex. 50 – 48 = 2 (2$ width of strikes) => 2$ *100 – 40$ (Premium Paid) – 5$ (Commission) = 155$ (max profit)

(a normal option contract controls 100 shares, therefore *100)

Maximum Loss: Premium Paid + Commissions

Ex. 40$ (Premium Paid) + 5$ (Commission) = 45$ (max loss)

Implied Volatility and Time Decay:

Just as a Bull Call Debit Spread the Bear Put Debit Spread also profits from a rise in implied volatility and therefore should be used in times of low IV (IV rank under 50). Doing this will increase your chances of winning.

The Time Decay or Theta is negative and doesn’t work in the favor of this strategy. The long option will lose some extrinsic value as time passes. It loses value at a faster rate the closer you get to expiration.

The Best Tool to Learn Options Strategies

If you want to learn much more about hundreds of options strategies, I highly recommend checking out The Strategy Lab. The Strategy Lab is a tool designed to help traders understand options strategies, options pricing and the options market in general.

I am very interested in Options trading and started to study it. I am still very new at it, and still having trouble understanding its complexity mainly due to many terminologies and how Option is priced.

But Options is the safe way to invest (I am not much of a risk taker here comes to the stock market) that you can put the hedge around the risk. I am looking forward to learning more about Options.

Hey Kyoko,

If you are interested in learning more about options and how to earn consistent money with them you should definitely check out my education section here.

Hi Louis

In the Bear Call and Bull Put Credit Spreads you identified the Break Even Point by a Formula such as: Short Strike – Net Credit or Short Price + Net Credit, Can please provide the formula for the Bull Call and the Bear Put Credit spread.

If possible can you elaborate in each of above strategies (Bull Call & Bear Put) where the profit exist above or below the BEP.

Thank you

Thanks for your comment Camille.

Here is a list of formulas to calculate the breakeven points of different spreads:

Bear Call spread: Short strike + Credit received (max profit is achieved if the underlying’s price is below the short strike)

Bull Call spread: Long strike – Debit paid (max profit is achieved if the underlying’s price is above the short strike)

Bear Put spread: Long strike + Debit paid (max profit is achieved if the underlying’s price is below the short strike)

Bull Put spread: Short strike – Credit received (max profit is achieved if the underlying’s price is above the short strike)

I hope this helps. Otherwise, please let me know.

Hi Louis,

Do you have any articles on debit call/put adjustments? I am familiar with turning a long into a vertical spread, turning the vertical into a butterfly if the underlying keeps going down or . But, wondering if there is anything different. Thank you.

Sadly, I do currently not really have any articles on option strategy adjustments. But I have written your suggestion down and I will create training on adjustments sometime in the future.

Hi Louis,

A bull call spread is an options trading strategy designed to benefit from a stock’s limited increase in price. The strategy uses two call options to create a range consisting of a lower strike price and an upper strike price.

Maximum gain is reached for the bull call spread options strategy when the stock price move above the higher strike price of the two calls.

My question: What I don’t understand is that:

– For a Single short call, if the stock price increases above the strike price, we make a loss. But in the above vertical spread, in fact we gain when the stock price move above the higher strike price of the two calls?

Hi Nicole,

Thanks for your question. A vertical spread consists of two options: a short option and a long option of the same type at a different strike price. For a bull call spread, you buy a call and sell a call at a higher strike price. This means that the long call option will be worth more than the short call option. Because of this, there is a certain price difference between the two options. If the underlying’s price moves above the strike price of the short option, you will be able to take advantage of this price difference because the long option will always be worth more than the short option. In other words, the long option is the dominant one and thus it has more influence on the payoff than the short option. Therefore, a bull call spread is a bullish strategy.

I really hope this helps.

Hi Louis,

Using this example, wouldn’t you still make money if the underlying goes past your short strike, because the long will gain in value faster than the short loses value if the underlying goes up in price? The long and short can’t be cancelling each other’s gain or loss exactly, correct? I ask because the payoff diagram shows the profit to stop at the short strike.

Thank you!

Hi Tim,

To calculate the break-even point of a bull call spread, you simply add the net cost of the spread to the lower (long) call strike. If the price of the underlying is anywhere above this price at expiration, the position will achieve a profit and vice versa. It is at this point that the long call’s gain and short call’s loss cancel each out exactly. Above it, the long call is worth more and below it the short call has a bigger loss.

I hope this answers the question. Otherwise, let me know.

Thanks for the super fast response. I think the only thing that I’m still confused with is the 1.) max profit calculation and 2.) the profit loss diagram.

1.) Max profit – your article states that Max profit = Strike of Short Call – Strike of Long Call (Width of Strikes) – Premium Paid – Commissions. This calculation makes sense if we are expecting to exercise both positions, or in other words calculating the instrinsic values. This calculation is not necessarily what the profit/loss would look like if we were just trading contracts due to option prices being different from stock prices, correct?

2.) Profit/Loss diagram makes sense if it is showing instrinsic value only.

Hi Tim,

The profit and loss diagram and the max profit/loss calculations are for the price of the position at expiration. So you are correct that they only show intrinsic value. At expiration, there is no extrinsic value left (because there is no time left till expiration). The blue line in the profit/loss diagram shows how the P&L looks sometime before the expiration date.

The formula to calculate P&L before expiration is much more complicated as you have to take many other market variables into account. If you are interested in such a formula, I recommend checking out my article on the black scholes formula.

If you have any other questions or comments left, please let me know.

Hello Louis, great explication abut this strategy.

the max loss that you defined for both is :Premium Paid + Commissions, that is because if the short side get ITM, you will get the premium, but the buyer can execute the contract, and that is nothing good, so you put a stop loss close to the strike price on the short side?

Hi Hernando,

I wouldn’t necessarily recommend putting a stop order at the short strike. Firstly, the odds of being assigned are relatively low. But even if the buyer exercised their option and you are assigned, your loss or gain isn’t affected significantly. This is the case because you have a long option to hedge the losses from the short position. So if you are assigned, you could just exercise your long option to close the assigned shares at the strike price of the long option.

I hope this helps.

Hi Louis, thanks for the reply.

So i have another questions, when you refer (Premium Paid) in the max loss for example, it mean that Premium Paid = Premium for long position (debit) – Premium for the short position (credit). The net value, this is correct?

Hi Hernando,

Yes, that’s right. By premium paid, I mean the net debit you paid to open the position.

sold 2 TSLA Jun 18 2021 1400Put @412.65 +82,526.85

Bot 2 TSLA Jun 18 2021 1700 Call @259.71 -51,943.33

Bot 2 TSLA Jun 18 2021 1200 Put @ 288.46 -57,693.33

Sold 2 TSLA Jun 18 2021 1500 Call @ 311.69 +62,335.29

this is an iron condor with over 300 days to expiry. Can you put this info in your spread chart and see if it looks correct?

Hi George,

Yes, that’s a short iron condor.

Say I own a debit spread, but realize that I may be leaving a lot of profit on the table as I now expect the underlying to make a massive move to the upside (say on a potential earnings announcement) much more than earlier thought.

Is there an adjustment to the debit spread I can make that will allow more upside potential gain instead of the difference of the two initial positions?

You could close the short position to turn the call debit spread into a simple long call. This will give you unlimited upside exposure. However, this will also move your break-even point higher and increase your risk.

How much time should one buy when planning a debit spread?

Lately I have been experimenting with ATM debit call and put spreads put on at the same time with the short sides 4 strikes away respectively buying back either short when it gets to 1/2 value, replacing it when it returns to original price. Maybe there is a name for this strategy I dont know.

Id like to go at least 3 months out in time but would the additional time cause a slower breakdown in value of the short option compared to something 50 days out? Not sure how to calculate that.

Lately I have been experimenting with ATM debit call and put spreads put on at the same time with the short sides 4 strikes away respectively buying back either short when it gets to 1/2 value, replacing it when it returns to original price. Maybe there is a name for this strategy I dont know.

Id like to go at least 3 months out in time but would the additional time cause a slower breakdown in value of the short option compared to something 50 days out? Not sure how to calculate that.