When trading, things sometimes don’t turn out to go entirely according to your plan. But what do you do if this happens? Do you sit tight and wait, close the trade or do something else?

In this article, you will learn about a few options adjustment strategies that will help you deal with struggling options trades. These adjustment techniques will help you minimize your risk without eliminating the potential for profit.

Options Adjustments Video Guide

Check out the following video in which I go through the best options adjustment strategies.

General Adjustment Guidelines

Before we get into any specific options adjustment strategies, I want to start by presenting a few general principles to always follow when adjusting your positions.

1. The entry trumps any adjustments

This first point isn’t really an adjustment principle. Instead, it is a general trading guideline. In my opinion, the most important part of

In other words, a good trade setup and entry is far more important than any trade adjustments.

2. Have a clear plan

The next adjustment guideline to follow is to always have a plan for when to adjust your position before putting on a trade. Your plan should answer all of the following questions:

- Will I adjust this position if it goes against me? For some options strategies, it might not necessarily make sense to adjust the trade at all. Sometimes, taking a small loss can be superior to any adjustments. But it is important to decide this before putting on the trade.

- At what point will I adjust it? If you decide that you want to adjust your trade if it goes against you, you need to set a clear adjustment point. This adjustment point could be a price level of the underlying asset, a certain delta value, an implied volatility level or something else.

- How will I adjust it? Last but not least, you should also plan how you potentially will adjust the trade. Here you don’t have to know every single detail, but you should definitely have an idea about how you will adjust the position if it reaches your adjustment point.

3. Don’t jump the gun

This guideline is about where to set your adjustment point. You should not adjust your position extremely aggressively. You should not adjust your position as soon as it goes slightly against you. Give your trades some room to breathe.

One reason why you shouldn’t adjust your positions too quickly is that the probability of touch is about twice as large as the probability that an option will expire ITM. This means that most positions will be tested at some point before their expiration. I recommend checking out my article on options trading probabilities to learn more about the probability of touch and the probability of ITM.

4. Decrease risk

A common adjustment mistake is taking on additional risk. But this does not really make sense as the entire point of adjusting a position would be to limit your downside potential while still leaving some room for the upside. If your trade is riskier after an adjustment than before an adjustment, I would not consider the adjustment successful.

An example of a good adjustment would be one in which you do not increase the risk, but you give yourself more time to be right. Another good adjustment of a losing trade could be one in which you move the breakeven point further out without increasing the risk.

To prevent increasing the risk, I usually recommend only adjusting if the entire adjustment can be done for a net credit. But more on this later.

5. Efficient capital management

Before adjusting a position, always ask yourself if this adjustment is the most efficient way to allocate your capital. Usually, an alternative to an adjustment would be to simply close the position and open an entirely new position.

So before adjusting a struggling trade, ask yourself where your money will do more for you: in a new trade or in an adjustment of this trade. It only makes sense to adjust a position if the capital allocated to it will be at least as efficient as a new trade.

Options Adjustment Strategies

Now that we covered some general adjustment guidelines, let us move on to some specific options adjustment strategies.

How to adjust an Iron Condor

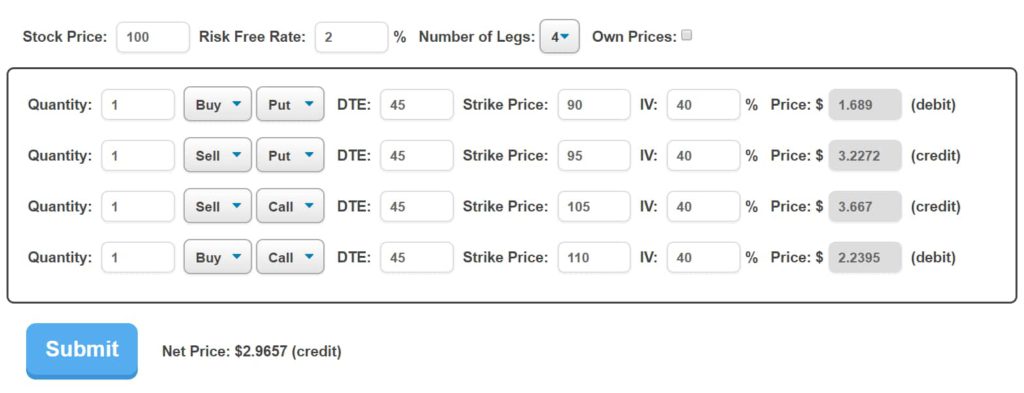

Let me start by presenting an options adjustment strategy for the defined risk and defined profit strategy, short iron condor. A short iron condor is a neutral, range bound option strategy that achieves max profit if the underlying asset’s price is between the two short strikes at expiration.

The following image is an example of how you could set up an iron condor:

This iron condor was set up in The Strategy Lab.

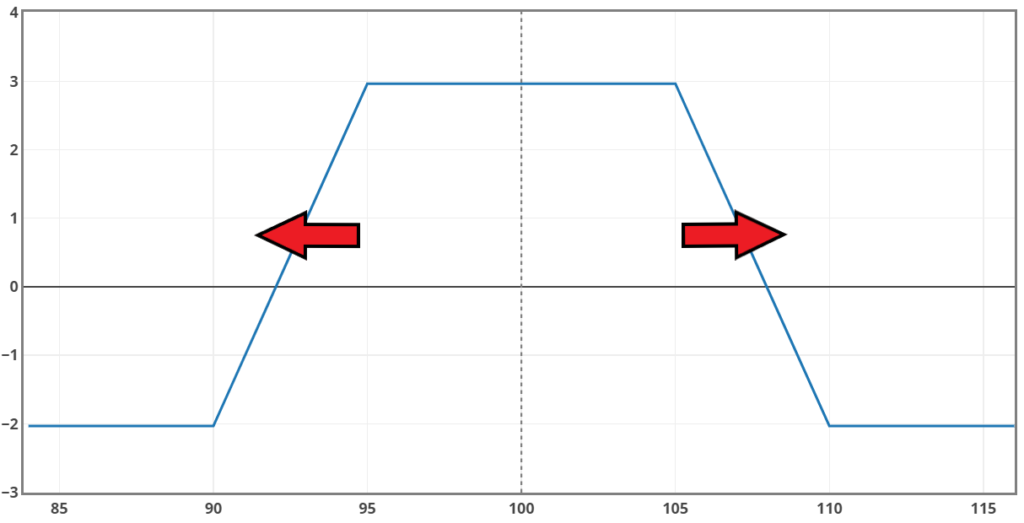

First, it is important to understand when you even should consider adjusting an iron condor. In my opinion, it would only make sense to adjust an iron condor, if the underlying’s price breaches either the upper or lower leg of an iron condor. I would not recommend adjusting an iron condor if the price stays in between the two short legs.

The following image shows the payoff diagram of the iron condor that we just set up. The two arrows indicate potential adjustment points.

The most intuitive way to adjust an iron condor would be to move the tested side further away from the underlying asset’s price so that the breakeven point is further out.

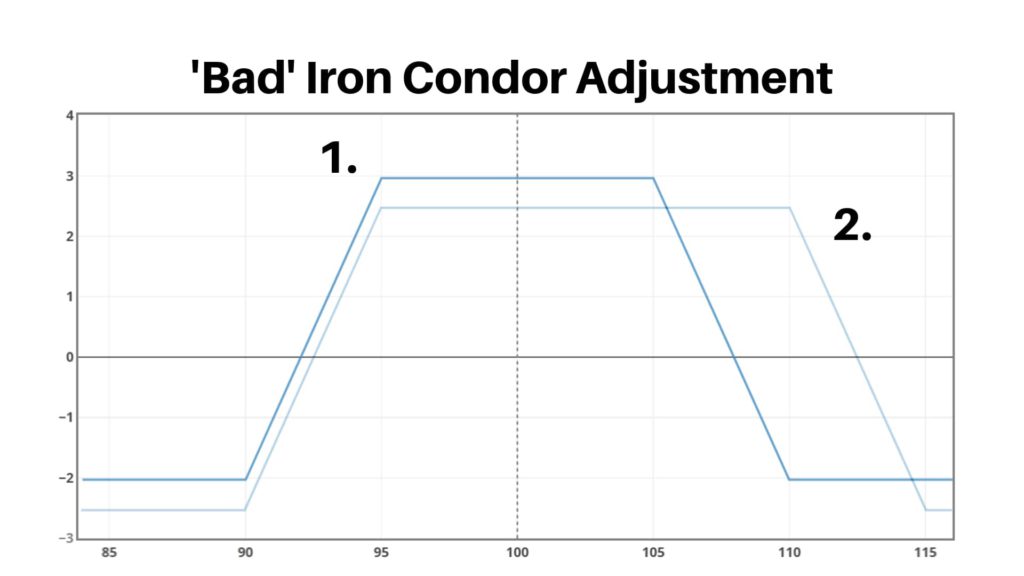

Let’s say that the underlying price for the just-shown iron condor moves up and beyond the upper short strike price. Therefore, we close the short 105 and long 110 call options and sell a new call at the 110 strike price and buy one at the 115 strike price.

If you make this adjustment the new payoff profile of our iron condor will look as follows:

- is the original payoff profile.

- is the new payoff profile.

As you can see, the new upper breakeven point is much higher than the original one. HOWEVER, the profit potential dropped and even worse, the total risk increased! This is a direct violation of the 4. adjustment principle that we defined earlier in this article.

Even though it is definitely possible to adjust an iron

So what should you do instead?

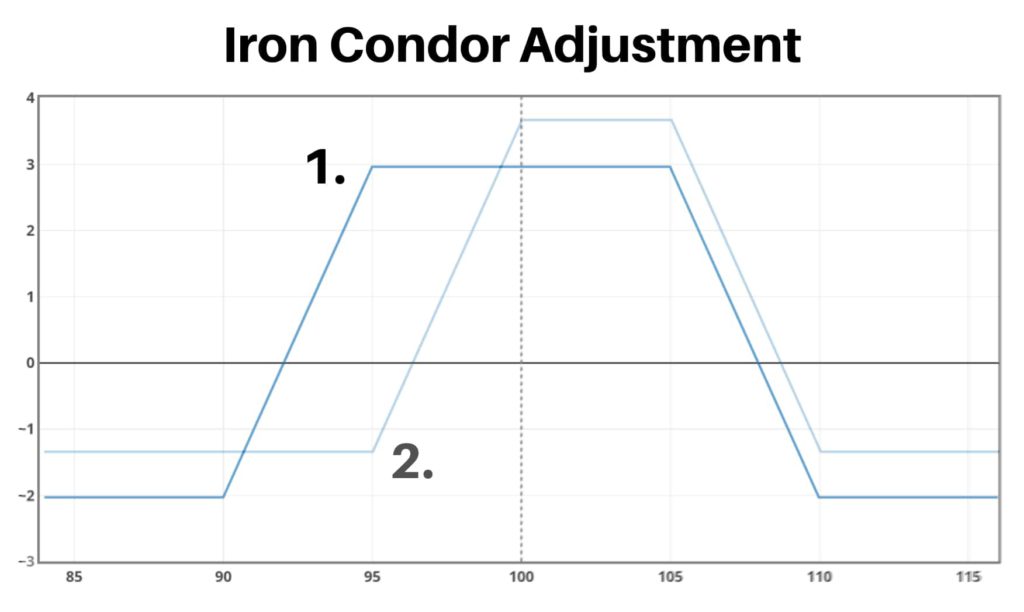

A better way to adjust an iron condor is to move the untested side closer to the underlying asset’s price. If the underlying’s price breaches one side of an iron condor, you usually aren’t worried about the other side. Furthermore, the other side normally won’t be worth a lot anymore as it will be quite far OTM.

This iron condor adjustment technique takes advantage of exactly this. It allows you to take profits in the untested side and collect additional premium by selling a new side closer to the underlying’s price. This won’t only decrease the overall risk and increase the profit potential, but it will also move the breakeven point further out.

In other words, it’s a win-win-win situation.

This is how the original payoff profile (1.) looks compared to the adjusted payoff profile (2.).

The only real disadvantage of this adjustment technique is that the profitable range becomes smaller. So if the underlying’s price comes all the way back, it might not be ideal. However, otherwise, it certainly outperforms an unadjusted iron condor.

The great thing about this adjustment technique is that you could theoretically repeat it over and over again as long as you still are able to collect enough premium. If that’s the case, you could decrease your risk, increase the profit potential and move out the breakeven point again and again…

An Example:

You sell the following iron condor on ABC which is trading at $50 at the time of entry:

- 1 long 40 put

- 1 short 45 put

- 1 short 55 call

- 1 long 60 call

Now ABC’s price drops down to $42 which is your adjustment point. The adjustment would be to move the call options lower. This can be done by closing both call options and then selling the 50 call option and buying the 55 call option. The new iron condor would look like this:

- 1 long 40 put

- 1 short 45 put

- 1 short 50 call

- 1 long 55 call

Let’s say you could make this adjustment for a net credit of $0.5. This would mean that the max loss decreased by $50 and the max profit increased by $50. Furthermore, the lower breakeven point was moved lower as well.

What about straddles and strangles?

This iron condor adjustment technique can also be used for other options strategies such as short straddles or short strangles. All you have to do is close the untested side and sell a new option closer to the underlying asset’s price.

Generally, just make sure to leave some room for the underlying price to move in. Don’t adjust too quickly and don’t adjust too aggressively!

What is going inverted?

If you repeat the just-presented adjustment technique over and over again, your put strikes will move closer and closer to your call strikes. At one point, the short put strike might even become the same as the short call strike. If this is the case, you won’t be able to repeat the adjustment again for iron condors as you won’t be able to make the adjustment for a net credit.

But if you are trading strangles (or straddles), you will still be able to continue moving up the put side (or moving down the call side). This would lead to your put strike being higher than your call strike. This is also known as ‘going inverted’.

Let me explain this with a brief example. Let’s say you sold a strangle on XYZ which is trading at $100 with the following strikes:

- 95 put

- 105 call

Now XYZ’s price moves up and beyond $105. Therefore, you buy back the 95 put option and sell a new one at the 100 strike price. Your new strangle looks like this:

- 100 put

- 105 call

XYZ’s price rises even more. So you decide to roll up the put option once again. The new strangle has the following strikes:

- 105 put

- 105 call

XYZ’s price continues to rise even further. Thus, you do the same adjustment one more time. Now your position looks as follows:

- 110 put

- 105 call

Now you just went inverted because the put option’s strike price is higher than the call option’s strike price. There usually isn’t something wrong with going inverted. Just make sure to collect enough premium to make the move worth it.

You can’t go inverted for iron condors or other defined risk strategies as you won’t be able to do this for a net credit.

How to Adjust Credit Spreads

We can use the same approach as we used to adjust iron condors for credit spread adjustments. One great way to adjust credit spreads is actually to turn them into iron condors. From there on you will be able to use the above adjustment method for any further adjustments.

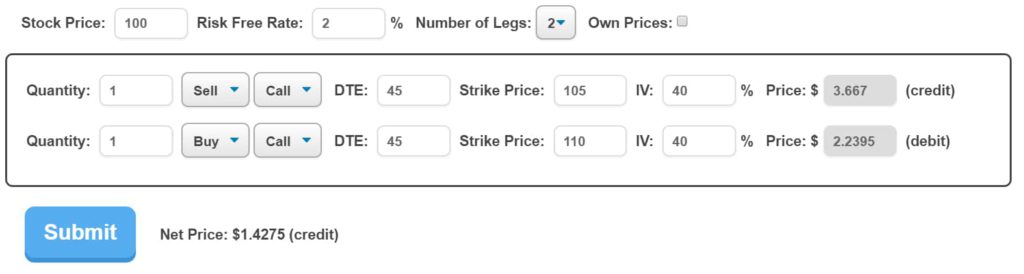

Once again, we do not touch the tested side of the strategy. Just like last time, I will present this options adjustment strategy with an example. The following image shows which short call vertical spread we will use for this example:

Similarly to before, a good adjustment point for credit spreads is when the underlying’s price breaches the short (or long) option. In our example, we assume that the underlying asset’s price moves up to about $108 (which is right between the short and long strike price).

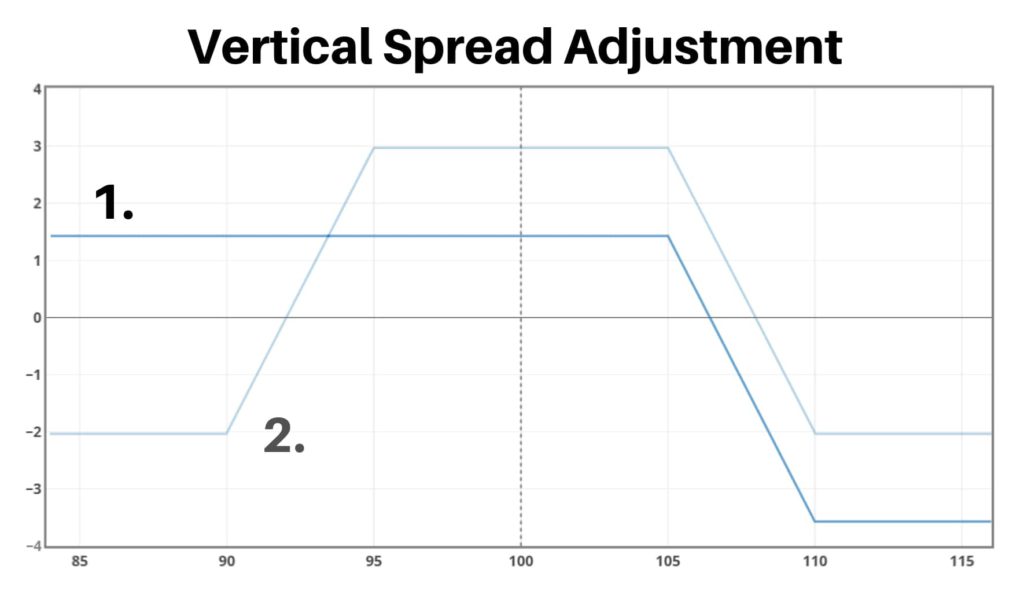

Now we sell a second put vertical spread to turn the original position into a short iron condor. The following graphic shows how the payoff is affected.

- is the original short call spread

- is the new short iron condor

As you can see, our adjustment, once again, significantly decreased the overall risk, increased the profit potential and moved out the breakeven point of the call side. The new position looks like this:

- long 90 put option

- short 95 put option

- short 105 call option

- long 110 call option

After this initial adjustment, you could theoretically, move up the untested side, if the underlying’s price continues to rise (and you are able to collect enough premium).

Like I said before, don’t be too aggressive with these options adjustment strategies. Give the underlying’s price some room to move in. You don’t want to sell the put spread too close to the underlying’s price. Otherwise, a big price reversal could hurt you.

Adjusting for Time

So far, we have only discussed options adjustment strategies that decrease your risk and increase your profit potential. In addition to these adjustment strategies, you can also adjust your positions for more time. The advantage of adjusting for time is that you give the underlying’s price time to come back into the profitable range.

Keep in mind that when adjusting for time, we still want to consider the general adjustment principles defined at the beginning of this article. So we still don’t want to increase the overall risk of a position. In practical terms, this means that the adjustment has to be done for a net credit.

How to adjust for time?

The specific strategies to adjust a position for more time are relatively simple. All you do is close your current position and reopen the same position in a later expiration cycle. The only problem with this is that you often won’t be able to make this adjustment for a net credit. Therefore, you often have to change the strike prices in the new expiration cycle.

Let me give you a concrete example:

You sell the following strangle on ABC which is trading at $200:

- short 190 put option

- short 210 call option

- 30 days until expiration

Over the next 20 days, ABC’s price drops down to $185. This means that your strangle only has 10 days left until its expiration date and things aren’t looking great. Now, you could use the adjustment technique presented earlier in this article (where you move down the short call option). The problem with this is that, you likely won’t collect a lot of premium as there isn’t a lot of time premium left in the options.

So what you could do instead is close the entire position and look at the options in the next expiration cycle with about 40 days left until expiration. One way of doing things would be to sell the exact same strangle in this expiration cycle. However, often, you won’t be able to do this because you couldn’t do it for a net credit. If this is the case, you could either move the upper strike closer to ABC’s price or move both strikes.

For the sake of this example, we will say that we have to move down the call strike to close the previous strangle and sell the new one in the new expiration cycle for a net credit. So the new position looks as follows:

- short 190 put option

- short 205 call option

- 40 days until expiration

With this adjustment, you just gave your position 30 more days to work out without increasing the risk. Furthermore, this adjustment moved the lower breakeven point closer to the underlying’s price.

For which strategies can you extend time?

Once again, rolling should only be done for a net credit. Sadly, this limits the strategies which you can roll to undefined risk strategies. You usually won’t be able to roll defined risk strategies such as iron condors for a net credit. So this adjustment strategy is mainly for strangles and straddles.

When should you roll?

You should not roll too early or too late. If there still is a lot of time left until expiration, you could either just wait or use the previously presented adjustment method in which you just move the untested side closer to the underlying’s price.

In my opinion, a good time to roll your positions to the next expiration cycle is about one week before the expiration date. So in the week before expiration week.

Conclusion

Even though adjusting your struggling positions can improve your overall profit and loss, it is important to not overestimate the importance of adjustments. Adjustments can be great, but you should still focus most of your attention on the trade entry!

There are obviously many ways to adjust options strategies. But in my opinion, the options adjustment strategies presented in this article are some of the best. But feel free to incorporate other adjustment techniques into your trading as well. My advice for this would be to still follow the general adjustment principles that I outlined at the beginning of this article.

Furthermore, make sure to not adjust too aggressively. Always remember that it is quite likely that a trade will be a loser sometime before expiration. So just because a position goes slightly against you, does not mean that you should immediately make an adjustment to it.

Define a rational adjustment point and adjustment strategy as a part of a clear trading plan before opening a trade and then stick to this plan.

Generally speaking, undefined risk strategies are easier to manage than defined risk strategies. The tradeoff here is that undefined risk strategies are per definition riskier than defined risk strategies. So depending on your risk appetite, capital and other preferences, you might prefer one over the other. But I would not say that one is clearly better than the other.

All the strategy images and adjustments were taken from The Strategy Lab. The Strategy Lab is a tool that TradeOptionsWithMe recently developed to help traders deepen their understanding of the options markets.

If you want to improve your understanding of options, make sure to check out The Strategy Lab:

Thank you so much to the author who has written down this kind of such a beneficial article. This article opened my mind to the fact that I can still make good money with options trading. I actually quit trading a few months back because I didn’t know how to cope with the losing trades. But seeing this article now, I am motivated and I will make sure to implement these options adjustment strategies that you have written in the article

Hi Tracy,

I am very happy to hear that you learned something from this article. If you want to check out more of this kind of content, you could check out my free options trading courses.

This is a wonderful article that must be read by all traders. I must say that your article is really informative and helpful and your efforts in putting this article together to share with us is appreciated. I have really learnt something valuable today on the adjustment techniques will help me minimize my risk without eliminating the potential for profit in trading. Great job!

Thanks for the positive feedback. It’s great to hear that you enjoyed reading it and learned something new.

Thank you for this insightful and educative write up.

Though I have been trading stocks for some years now, I want to learn more about options. The Strategy Lab looks like a great tool to learn more about options strategies. I will reread this article again to better understand everything.

please I’m not very clear on the part of when to roll. How would I know I am not rolling too early?

I can’t give you an exact answer because when to roll can vary from situation to situation. Generally speaking, I would probably not want to roll earlier than three weeks before expiration. The idea behind rolling is to extend time, so if you still have a lot of time left until expiration, this adjustment doesn’t make that much sense.

I hope this helps. Make sure to let me know if you have any other questions or comments.

Thanks for writing this article on options adjustments. I must commend you for a job well done for taking your time to write this article. I really find it useful and am going to start applying it to my trading because I learn new things from it. Most time I discover that is the trade entry that determines my profit, although I do use adjustment and I must say it always a life saver. But no matter the adjustment, I will always advise to take profit when necessary no matter what

Thanks for sharing your thoughts. I agree that taking profits is an essential part of profitable trading.

Once again thank you for a brilliant informative article Louis. For me adjusting trades was one of the most confusing areas in my quest to master option trading. This article explains it in a logical way with proof.

If anybody was wondering, the Strategy Lab is worth every penny. The confidence I’ve gained by running different scenarios through it is priceless (when selling, adjusting and to plan the trade even before opening it). I can also see where past trades/adjustments hurt and where it worked.

Hi Johan,

Thank you so much for the positive feedback. It is great to hear that you enjoy my content.

Informative. Many IC adjustment approaches out there – some suggest buying back 1/2 of the short option that is causing grief, I suppose hybrid approaches could also be used?

Hi Steve,

There are many good adjustment strategies that aren’t mentioned in this article. These can often be combined to even better adjustments. I just recommend considering the general adjustment principles covered in this article when combining/using other option adjustment strategies.

I learnt a lot from this adjustment in example of Iron Condor .But please clarify as to how to calculate revised BEP on Put side and Call side. In Iron Condor example, as the price moves upward you adjusted Put credit . In this situation how to calculate revised Break Even Point and Profit and loss.

Thank you.

Hi Sohan,

Your broker platform should automatically calculate these figures. If it doesn’t, you could consider changing broker.

With that being said, this is how you would calculate the BEP of an iron condor per hand:

Lower BEP: Short put strike – net premium received

Upper BEP: Short call strike + net premium received

The max profit is the net premium collected and the max loss is the width of the call/put spread – net premium collected.

To account for the adjustment, you just need to change the put strike and add the extra net credit collected from the adjustment to the net premium received.

I hope this answers your question. Make sure to let me know if you have any follow-up questions or comments.

Thanks Louis for your prompt answer…

I have few questions for iron condor :

In one of the spreads , you showed us the calculation of prob of profit X profit and prob of loss X loss. Is it required to see in the case of iron condor also for more prob of success.

What is the adjustment if e.g call spread comes deep in the money as the market suddenly becomes bullish ?

Also Is there anything one should do if the one side

Spread crosses other side spread strike price ?

In selection of strike price what delta value one should consider for call and put ?

As iron condor is beneficial when market is in range bound. Is there any method by which one can determine that market is in range bound ?

Hi Sohan,

The calculation that you mentioned can be a good guideline for many strategies including iron condors. But note that it should only be used as a guideline. You should not base any trading decisions purely on the result of it.

The only adjustment I use for vertical spreads is to turn them into iron condors. They are a defined risk strategy and don’t need that much managing. Worst case scenario, you just cut the loss.

Depending on your market assumption and risk level, you could choose a higher or lower delta. A good conservative delta for the short call and put option is 0.3-0.4. But this also isn’t more than a rough guideline.

You could use technical analysis to try to determine if the market is in a channel. But I usually don’t do this. Instead, I just look for high IV securities on which I can collect a lot of premium. As long as you keep the range wide enough, the odds should be on your side.

I hope this helps.

Hi Louis,

Most of the time I have lost lots of my capital selling naked calls. Is there any guidelines as to when the position to be squared off when we are in loss ? Or else what should be the adjustment ?

I wait for the market to come in my favour but it seldom comes and when I book huge loss , the next day market reverse and I repent on loosing capital ? Any way out for this. I am reluctant to cut my loss. What should be the thought process and how to control emotion ?

Hi Sohan,

Firstly, you could trade defined risk strategies instead of selling naked options. This would dramatically lower your risk.

Furthermore, I recommend always setting a max loss tolerance before entering a trade. As soon as you reach this loss, just cut the loss. Setting a risk level before opening a trade allows you to stay rational.

For more on this, check out my trade entry and exit guide.

As for adjustments of naked options, you could turn them into strangles, or just roll them out into the next expiration cycle over and over again (as long as you can do this for a net credit).

hi Louis, I must say that your wonderful article is really informative and helpful. Now I have a question about adjusting the bad credit spread, still use your example, let’s say I miss the good adjusting point at $108, now the price going up to about $115 (now even through the long call strike price). So what will you do to adjust it? do you still short a put spread to make an iron condor? if so, what strike do you short? Thank you.

Hi Ben,

Thanks for the comment. When looking at possible adjustments, you always have to consider your directional assumption and what difference any possible adjustments can make. The worst-case scenario is that the price has moved too far for you to make any logical adjustments. Especially for defined risk strategies, this isn’t the end of the world. I’d recommend always looking at multiple different strike prices before adjusting. Here are a few things to consider when looking at different strikes:

1. How much extra premium can you collect?

2. How wide will your profitable range be with this strike price?

3. What’s your new POP?

Now weigh these different aspects to evaluate which strike price (if any) is the best choice.

What I don’t recommend doing though is going inverted (meaning that the put strike exceeds the call strike) with defined risk strategies.

I hope this answers your question. Otherwise, let me know.

Louis, Thanks for your prompt answer.

Since the price has moved too far to do good adjusting(make the iron condor), I am thinking how about roll the call credit spread up to near $115 (i.e. 110/115), it makes higher probability, but got me the negative premium, Is it good or bad?

Hi Ben,

If an adjustment is good or bad totally depends on your trading system and market assumption. I personally prefer to only do such adjustments for a net credit since I would otherwise increase my risk (and decrease my profit potential) which goes against what I am trying to do in the first place.

LOVED YOUR ARTICLE ON ADJUSTMENT STRATEGIES……VERY GREATFUL FOR SHARING THIS WONDERFUL INFORMATION….GOD BLESS

You’re very welcome.

Excellent video and notes on trade adjustments Louis. Your content offers the most simplified illustrations that help drive concepts home. I am learning strategies and moved away from naked calls to spreads, short strangles and ICs. But having to adjust is a reality and this guidance will help me. Are you considering any 1:1 coaching for a fee?

Hi,

Thank you very much for your positive feedback. I am very happy to hear that you like my content. As of right now, I am not offering personal coaching for a variety of reasons. But feel free to ask questions if you ever have any.

May I know what type of adjustment would you recommend when a Bull Call Spread is moving down? Should it be converted to an IC through Put spreads? Ex: MU- stock price was 37 when entered. Long Call 40, Short Call 45. Price dropped to 34.

Thanks for the question. Since bull call spreads are a net debit strategy, it can be hard to adjust them for a net credit. I do not recommend opening an additional bear put spread since this will totally change the payoff of the strategy and increase risk (since it is a net debit strategy). Since debit spreads are defined risk strategies (and relatively low probability trades), you could just not adjust such a trade at all.

One potential adjustment, however, would be to roll the short option closer to the long option (for a net credit). This reduces risk and can move the BEP favorably. But you have to look at the individual situation to determine whether this is worth it or not.

I hope this helps.

I bought a put on a stock that had just broken through and looked like it was heading farther down. As if on cue, it turned around and went up two points. My broker should let me write a put and turn that into a credit spread shouldn’t they. Cash, margin, account balance are not issues. I am down $41 as I bought at the exact worst time and the spread looks pretty good. Naturally I will watch the market tomorrow and see what the direction is; I just want to make sure I can write a put against a put that is already in my account.

Hi Jim,

Depending on your account type or broker trading privileges, you might not be able to sell options. If that’s not an issue, there should be nothing preventing you from doing so. As long as you don’t sell the exact same option, you can certainly create a spread out of your existing position.

In defined risk strategy like IC, if by adjusting we end up forming Iron Butterfly and if price moves further in one direction, we cannot further move untested side for net credit. In such scenario what is best further adjustment strategy?

Hi Harish,

If you can’t adjust for a net credit, I wouldn’t recommend adjusting at all. Sometimes trades don’t work out, even after adjustments. But especially for defined risk strategies this shouldn’t be too big of a problem since the max risk is limited.

Thank you so much. This article is an eye opener indeed. I have been into a help less situation few time when my trades went away from my control. Now I am sure that I will confidently approach to manage the risks in case my trade goes in the opposite direction of my plan. You have really helped to save money for many and imparted a great knowledge. I also liked your approach that you kept to stance to maintain the net credit all the time while discussing the adjustments.

Thank you for your feedback. I am very happy to see that this helped!

Love it’s a great article, been struggling with adjusting spreads.

Sir thank you for writing this Blog and this adjustments are clearly understand and very usefull to me.sir, same like this adjustments where will I get remains strategies adjustments.

Hi Louis

Thanks for wonderful techniques. I really loved the way you explain adjustments.

Can you give an example how to adjust a SHORT STRADDLE. It will be a great help.

Thanks

Hello Louis.

I love all of these articles, especially this one. I have been rolling

options the wrong way all along. This has been a real eye opener.

In your example you rolled/closed the untested side, normally

I would wait until the price closed above one of my short legs before

even considering rolling. Let me explain, if Im in a trade that

expires Friday of this same week and we are on Thursday and the

price closes above the call side at 4pm. When the market opened

Friday morning is when I would roll the tested side.

Now when you roll the untested side,

1) Do you keep the same expiration?

2)What about premium if you are rolling on the same expiration date?

3) How much time do you wait before you decide to roll?

Thanks