The calendar spread options strategy is very widely used and has its special kind of purpose. It is often used to balance out portfolios because with it, it is possible to target specific strike prices. Here you will get a calendar spread explained:

Market Assumption:

The beauty of the calendar spread trading strategy is that it can be used for almost every direction. For a neutral, bullish or bearish market outlook. With calendar spreads you try to target one specific strike which can be as far OTM or close to the market as you desire. This is also the reason why this strategy is so great to balance out portfolios.

Setup:

- Sell 1 Call (at whatever strike you want to target)

- Buy 1 Call (at same strike), the expiration for this long Call has to be at a further away expiration date than the expiration date of the short option (ex. expiration 1 month later)

or

- Sell 1 Put (at whatever strike you want to target)

- Buy 1 Put (at same strike), the expiration for this long Put has to be at a further away expiration date than the expiration date of the short option (ex. expiration 1 month later)

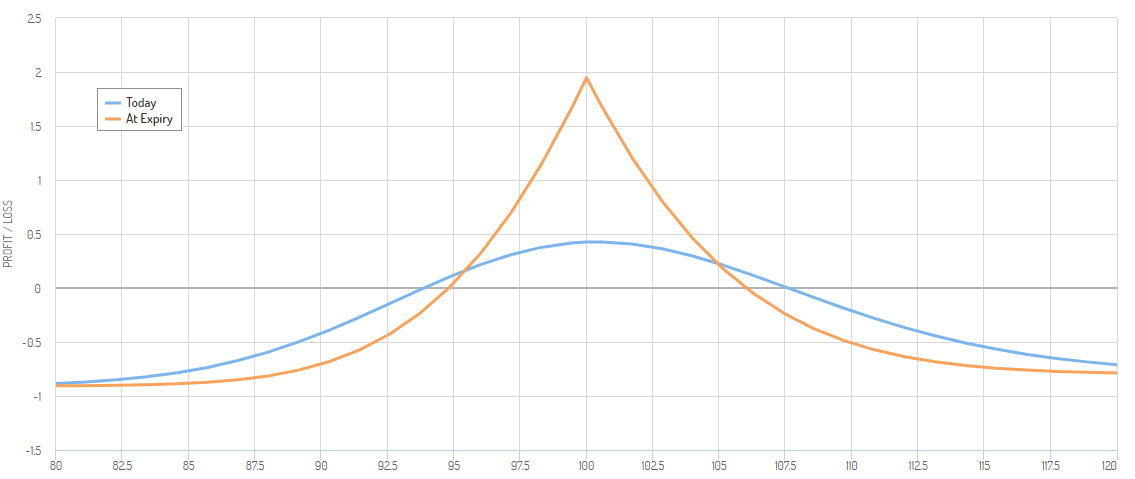

Profit and Loss:

A calendar spread is a defined risk strategy with a limited upside as well (until expiration of the shorter term option. If that expires worthless you are left with a long call or put with unlimited upside and defined risk). The maximum profit of the original strategy is rarely hit perfectly because to reach max profit the underlying price has to be at one specific strike. It is very difficult to predict this specific price and therefore max profit isn’t reached too often. But this strategy still profits when the price is near the targeted strike or if implied volatility rises enough. Max loss occurs when the price is far enough away from the targeted strike. The main profit of this strategy comes from the different rate of time decay of the two options. The short option is nearer to expiration and therefore ‘gains’ (sold option loses) value faster than the long further away option loses value.

Implied Volatility and Time Decay:

This strategy can profit quite a lot from a rise in volatility because the back month long option will gain in value when IV rises. Therefore, the calendar spread option strategy logically should be traded in times of rather low volatility (under IV rank 50).

Until the expiration of the first contract time decay or Theta works in favor of this strategy. This is because the sold front month option loses value faster than the further away long option. This is what the whole strategy is based on. But after the expiration of the short option a calendar spread will turn into a long call or put (depending on what you used) and a normal long option loses value from time decay. So Theta then turns negative.

Thanks for this information!

This field is all new to me, and it was an interesting introduction to something i previously know nothing about.

At the moment, I am targeting other projects, but i have been thinking of looking into options in the past, and might actually now do so, and i will defiantly check your site out for reference.

thanks,

kevin

Hey Kevin,

Sounds Great! To learn more about options you could check out my education here.

I have always been interested in stocks and this article opens my eyes to a new strategy. I love learning about new strategies and I have never seen this one so I am looking forward to researching it and learning more about it to implement it. Thanks as well for communicating the risk for this strategy and not just advertise the upside.

Hey Austin,

I am happy to help. If you want to learn even more option trading strategies, similar to this one I’d recommend the strategy section on my site. You can find it here.

Hi Louis ,

I have applied diagonal spread with short OTM call of current week and Long OTM call of monthly expiry.

If the market goes down I will be in profit but if the market goes up then how to adjust such position ?

Regards,

Sohan

Hi Sohan,

I can’t give you any specific advice since I can’t assess your position from the information given. But generally, I try to be conservative with my profit target on calendar spreads. That means I aim for about 1/3 to 1/2 of max profit.

One possible adjustment would be to roll down the short call position. But if you do this, make sure to collect additional premium so that you decrease your overall risk and move your breakeven point(s) in your favor.

I hope this helps.

I sell options and therefore complete knowledge of adjustments is required.

Hi,

You could check out my options trading adjustment guide. I hope that helps.

Let me know if you have any other questions or comments.

thanks