Bonds can be an excellent investment vehicle. Sadly, they are often misunderstood and thus many investors don’t take advantage of the potential that bonds offer. Even if you aren’t interested in actually trading bonds, it can be of great use to understand the bond market and its relation to other markets such as equities.

In this article you will receive an answer to all of the following questions:

- What is a bond?

- How does a bond work?

- What types of bonds exist?

- What are the differences between bonds and stocks?

- …

Video Breakdown of Bonds

Check out the following video in which I cover everything you need to know about bonds:

What is a Bond

When a company needs capital, they have multiple options. For instance, they could get a loan from a bank or issue more shares. A popular alternative to these two methods is to issue a bond. Bonds allow companies to borrow money from the public. One advantage of issuing bonds over issuing more shares is that they don’t have to give up any equity (ownership rights). Furthermore, bonds often have lower interest rates and can be cheaper than bank loans (for companies).

Just like with a normal loan, the company will pay interest to the buyers of their bonds. Furthermore, they promise to pay the borrowed money back after a certain time-frame.

Bonds can be issued by companies or even by government entities.

How Does a Bond Work

Bonds work very similarly to normal bank loans. The following list summarizes some of the key features of bonds:

- Face Value: The face value is also referred to as par value. This is the value of the bond when it is first issued. The most commonly used face value is $1000.

- Coupon Rate: The coupon rate is the yearly interest rate paid by the bond. Just like with normal loans, these interest payments are usually paid at regular intervals (e.g. once or twice per year). Typically, the coupon rate does not change.

- Maturity: Just like all loans, bonds also have an expiration after which the bond issuer has to pay back the borrowed funds. This time-frame is also known as maturity. The maturity of a bond can vary widely. It can be shorter than a year or as long as 30 years.

- Price: The price is not the same as the face value. Just like stocks, bonds can also be bought and sold after they are issued. The face value refers to the value of the bond at issue, whereas the price refers to the money that you could currently buy or sell the bond for.

- Yield: The yield of a bond takes into account the current price of a bond and its coupon rate. The yield is typically calculated by dividing the coupon rate by the bond’s current price.

Hopefully, this gives you an overview of how a bond works. Next up, I will discuss some of the risks associated with bonds.

The Risks of Bonds

Just like stock prices, bond prices also change. One of the main factors influencing the price of a bond is how its yield compares to that of similar bonds. For instance, if the yield of one bond is much lower than that of other bonds, fewer people will want to buy this bond which will likely lead to a drop in its price.

However, if you are planning on holding a bond until its maturity, these price fluctuations won’t affect you. You will still receive the same sized interest payments as you normally would. Furthermore, no matter what the price is, you will be paid back the face value of the bond at maturity.

Longer maturity bonds usually have higher yields because they are more exposed to changes in interest rates. But more on shorter vs longer term bonds later.

As bonds don’t give you any equity, a bond gives you no direct exposure to a company’s stock price.

The main risk of bonds is that the issuer will default. If this happens, the bond issuer won’t be able to meet their obligation to pay back the borrowed money. Depending on the bond, this risk can be very low to moderately high. Riskier bonds usually also have higher coupon rates. The bonds with the lowest default risk are those issued by stable governments.

For instance, US Treasury bonds (issued by the US government) are considered some of the lowest risk financial instruments because it is very unlikely that the US government will default. With that being said, very low-risk bonds such as US Treasury bonds also have low yields. For example, at the time of writing this, US Treasury bonds have a yield of under 3%.

How Does a Bond Work – Example

To make how a bond works as clear as possible, let me outline the entire process from issuing the bond to its expiration with an example:

Company XYZ needs $1’000’000 to finance one of its newest projects. They don’t want to give up any of their equity which is why they don’t issue more shares. Instead, they have decided to issue 1000 5-year bonds with a face value of $1000. The coupon rate is 7% and the interest payments occur semi-annually.

You decide to buy two of these bonds for $1000 each. If you hold these bond until maturity, you will receive $70 twice a year for the next five years. As long as company XYZ does not default, you will be paid back the entire $2000 that you paid for the two bonds after 5 years. This means that you will have made a total profit of 5 * $140 = $700 on a $2000 investment after 5 years.

Alternatively, you could also sell the bond sometime before maturity. If you do this, you won’t receive any further interest payments. The price at which you will be able to sell the bond depends on a variety of factors. The biggest factor is the coupon rate of comparable bonds. If the yield of XYZ’s bond is relatively low, you might not be able to sell the bonds for $1000 each. However, if XYZ’s bond yield is relatively high compared to similar bonds, you might even be able to sell the bonds for more than $1000 each.

How to Trade Bonds

Just like stocks, there are multiple different ways to trade bonds. Probably, the most common way to trade bonds is just to buy and hold them for their interest payments. If you buy and hold a bond until its maturity, you won’t be exposed to the changes in the bond’s price. You will only be exposed to the risk that the borrower will default and changes in interest rates.

To clarify this let me give you an example. Let’s say you buy a $1000 10-year bond with a coupon rate of 3%. This would mean that you will receive 3% of $1000 ($30) every year for the next 10 years. Over the next few years, interest rates go up and other similar bonds have coupon rates up to 6%. This makes your bond look much less attractive than before. Now you have two options:

- Just hold on to the bond until maturity.

- Sell the bond. However, as your bond has a much lower coupon rate than other comparable bonds, you likely will only be able to sell it for less than $1000.

Hopefully, this example clarifies how bonds’ prices can be affected by changes in interest rates. This exposure to interest rates is higher for longer term bonds because interest rates are much more likely to change in a long time period than in a short one. To compensate for this, longer term bonds often have higher coupon rates. But more on this later.

An alternative trading style to buying and holding a bond is to bet on the price fluctuation of the bond. If you are doing this, you are mainly betting on the changes in interest rates.

Generally speaking, bonds are a great investment vehicle for diversification. Depending on the bond, they are relatively low-risk vehicles with predictable behavior.

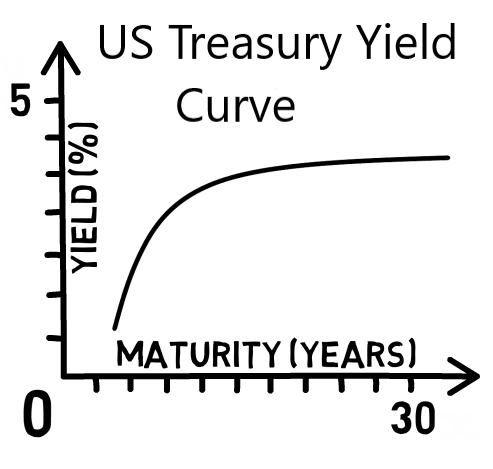

The Yield Curve

Another important topic related to bonds is the yield curve. Investors often consider the yield curve to be one of the best indicators for upcoming recessions. But what exactly does the yield curve tell you?

The yield curve plots the relationship between the maturity and yield of different bonds. It is possible to create a yield curve for almost any type of bond.

But the most famous and arguably most important yield curve is the one that plots this relationship for US Treasury bonds. The normal shape of the yield curve can be seen in the following graph. The short term bonds offer the lowest yield and the long term bonds offer the highest yields.

Longer term bonds tie up your money for a long time period. It is much likelier that interest rates will change in 10 years than that they will change in 1 or two years. That’s one of many theories trying to explain why long term bonds tend to have higher yields than short term bonds. Since bond prices change, so do their yields and thus, this relationship is subject to constant changes.

For instance, it has become a repeating pattern that leading up to market downturns and recessions, the yield curve has begun to flatten and even invert. Especially the spread between the 2 year and 10 year yield is very closely watched. If it inverts, many investors see it as a signal for an upcoming recession.

What an inverted yield curve actually means is heavily debated. But in simple terms, it means that more people buy long term bonds which pushes their price up and thus the yield down. This is typically the case when investors feel that the short-term outlook is very bad and they are therefore willing to accept lower yields for long term consistency.

So as an investor, it is a good idea to keep always one eye on the yield curve and if it inverts be extra cautious.

Different Types of Bonds

Now that you know what bonds are and how bonds work, let me present some of the different types of bonds that exist:

US Treasury Securities

Treasury securities are considered one of the safest investment in existence. The reason for this is that they are backed by the US government as the issuer of these bonds is the US Treasury. Furthermore, they are very liquid.

But as these bonds are very safe, they have some of the lowest yields out of all bonds.

There are three main types of US Treasury securities:

- Treasury Bills (T-Bills): These are short term zero-coupon bonds. They have life spans from only a few days until one year. Zero-coupon means that they don’t pay any interest. Instead of receiving interest payments, you will be able to buy T-Bills for a discount.

- Treasury Notes (T-Notes): These are medium term bonds with maturities from two to ten years. The interest payments for Treasury notes occur semiannually (twice a year).

- Treasury Bonds: These are very long term bonds with a maturity of 30 years. Treasury bonds also pay interest twice a year.

Different than many other bonds, the minimum investment for US Treasuries is only $100 (instead of the more common $1000).

Corporate Bonds

Corporate bonds are the bonds issued by companies that need money and don’t want to get a loan from a bank or issue new shares. Different than buying stock, buying corporate bonds does not give you any ownership rights in the company. You are simply lending the company money.

The specifics of a corporate bond vary from company to company. The maturity generally is as short as a year or as long as 30 years. The coupon rates can also vary widely depending on the type of company, industry and much more.

Most of the time, the minimum investment for corporate bonds is $1000.

Municipal Bonds (Munis)

Municipal bonds are issued by governmental entities such as states and cities. They are used to raise money for public projects (e.g. for schools, roads, general infrastructure…). These bonds can vary greatly in quality, liquidity, risk, coupon and maturity.

Some municipal bonds have maturities up to 30 years, whereas others have maturities of only a few years. Furthermore, some municipal bonds are zero-coupon bonds (issued at a discount) and others have regular interest payments.

The minimum investment for municipal bonds usually is $5000.

International/Foreign Bond

In addition to the bonds mentioned so far, there also exist non-US bonds. Most countries have their own set of bonds that can be issued by a country’s government, by companies in the country and more. Buying foreign bonds can be a great way to further diversify your portfolio as they allow you to gain exposure to other countries/economies.

Depending on the state of the different country/company, the risk and yield can vary widely. Generally, all the specifics for the different foreign bonds can differ a lot. However, the overall structure of these bonds should be very similar to that of US bonds.

As most foreign bonds pay interest in the country’s local currency, foreign bonds also expose you to currency risk. This is the risk that the local currency can increase or decrease in value compared to the US Dollar.

Besides the types of bond just presented, there also are some other (less popular) types of bonds that I won’t cover in this article.

The tax laws for bonds highly depend on the type of bond that you are trading. For instance, the interest payments that come from US Treasuries are only subject to federal income tax, whereas interest payments from corporate bonds are subject to both federal and state income tax.

Usually profits and losses that come from selling a bond are taxed in the same way as profits and losses from stock trades.

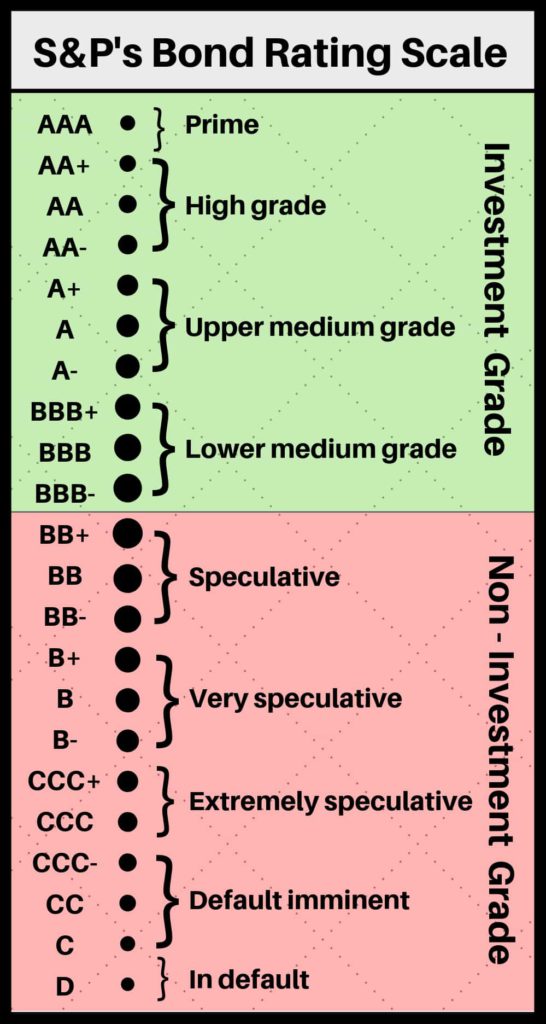

What are Investment Grade Bonds

Corporate and municipal bonds are subject to so-called credit ratings. These credit ratings are performed by credit rating agencies. The three biggest and most well-known credit rating agencies are:

- Fitch

- Moody’s

- Standard and Poor’s

These are also known as the “Big Three” credit rating agencies.

These rating agencies rate the credit risk of different bonds and rank the bonds into different categories. The categories vary from rating agency to rating agency. To explain the different categories, I will use the Standard and Poor’s rating scale.

This is how S&P’s rating scale looks like:

Bonds that are rated AAA are usually very high-quality bonds that have a very low risk of default. These bonds are also referred to as prime. The further down the scale you go, the higher the rated risk of default becomes.

There are two overall categories when it comes to bond ratings:

- Investment Grade: Investment grade bonds are those with a rating better than BB+ (and better than Ba1 on Moody’s scale). These are usually considered relatively safe, high-quality investments with a low risk of default. The yield of investment grade bonds is normally relatively low.

- Non-Investment Grade (Junk Bonds): These are the bonds that have worse ratings and thus don’t make it into the investment grade category. To compensate for the added risk, junk bonds have higher yields which is why they are also known as high-yield bonds.

After bonds have been issued, their rating can still change. The price of a bond can be severely impacted by a change in its rating.

Government bonds such as US Treasuries aren’t subject to these ratings. But they are considered to be of the highest quality (AAA).

Note that there have been multiple scandals with credit rating agencies in the past. For instance, in the aftermath of the 2008 financial crisis, rating agencies have faced severe criticism as a lot of their ratings have not been objective which, today, is considered one of the causes of the 2008 crisis.

Stocks vs Bonds

Stocks and bonds are two entirely different investment vehicles. Stocks give you ownership rights in a company (equity), bonds don’t. Bonds are debt obligations that are used by companies and governments as an alternative to issuing shares and loaning from banks.

Generally speaking, bonds are much less volatile and also less risky than stocks. But this highly depends on the bond. For example, US Treasuries are considered the safest investment in existence as they are backed by the US government. This means that the risk of a US Treasury bond is that the US government will default which is very unlikely.

On the flip side, the returns of bonds are usually also lower than those of stocks.

As bonds offer exposure to very different factors than stocks, bonds and stocks are quite uncorrelated. Therefore, a combination of bonds and stocks can be a great way to diversify your portfolio.

Conclusion

Bonds are a great investment vehicle with relatively low risk and low volatility. They can be a great way to further diversify your portfolio.

However, just like with all investments, it is very important to do your research before investing any money into bonds. The exposure and risk that different bonds offer can vary widely. So make sure to be aware of the risks before risking any hard earned money.

I really hope that this article helped you understand how bonds work. I would love to hear if you are planning on adding bonds to your future investment arsenal, in the comment section below.

If you want to learn more about the markets and different trading opportunities, make sure to check out some of our other trading posts.

Hi Louis,

I think I will visit your website more often. You demonstrate good understanding of bonds. Personally I prefer Treasury bonds, unlike Corporate bonds where you the risk of default can be high unless you have good research skills and time to follow up on the Company performance, leadership changes and competition. It is also much easier to sell Treasury bonds, and you can use them as collateral when applying for funding – when you need capital to start a business.

Foreign bonds pay good interest, but with some countries going through some political instability or change in governments, it maybe a challenge to predict the policy direction. This is a very interesting topic.

Best Wishes,

Sandikazi

Hi Sandikazi,

Thanks so much for sharing your thoughts about the different types of bonds. I agree that Treasury bonds are probably one of the best investment vehicles for those that don’t have the time or will to do the research required to successfully trade other bonds or stocks.

Thank you for the thorough article. I think investing is thinking about our future so I’m always interested in different possibilities. Your guide has given me useful information. Do you think that investing in bonds is less risky than in cryptos? My husband believes that the best investment is a real estate investment. What do you think? I’ve also read that gold is a good investment nowadays as well. Are bonds rated AAA offered for foreigners as well?

Hi Agnes,

Let me start with your question about the risk of bonds vs the risk of cryptos. The answer to this question really depends on the bond. There certainly are some bonds that are much less risky than cryptocurrencies (e.g. Treasury Bonds). However, other high yield bonds might be just as risky.

Sadly, I am not very experienced with real estate, so I can’t really tell you too much about it. But just like with most investments, as long as you do your research and have a good understanding of what you are doing, real estate offers great investment opportunities.

Furthermore, I currently don’t have a certain directional bias on gold.

It doesn’t really matter where you are from when it comes to the markets. You can easily invest in (US) AAA-rated bonds even if you don’t live in the US.

I really hope this helps.

Hey there!

Wow! I have to must say that it’s really a nice article about bonds. Actually, U don’t hear anything about the bonds before. So, it’s a really new topic for me. But I’m very curious to learn more about the bonds. So, I’d read your article fully and researched it google. I don’t think so it’s so risky. It is a great investment vehicle.

But it’s don’t give me ownership in a comoany. So, can you tell what’s the reason about it? I want to know.

I’m gonna share this article with my friends. Thanks again for sharing this with us.

Thanks for your comment. Bonds don’t give you ownership rights in a company because they are debt obligations. In other words, they are a very similar alternative to bank loans for companies that need capital.

If a company wanted to give away ownership rights, they could issue (more) shares.

Hopefully, this answers your question.

Hey Louis,

This is really an unique and informative article. I had heard about bonds before but did not have proper knowledge about it. But as I am interested in stock marketing I searched a lot about it. And after reading your article is come to know many things and the concept about it became more clear. Moreover I have understood the difference between bonds and stocks. As bonds are more low risky and low volatility and you have given a proper guideline about it. I now have a much better understanding of how bonds work.

Thank you for writing such a helpful article.

I am very happy to hear that you enjoyed this guide to bonds and learned something new.

Seems like the good old risk/reward factor in operation here. For me, it would all be about interest and definitely the credibility of the company before I would make an investment. The higher the interest, the more I would make in return, but I saw the example where if the bond’s interest went from 3% to 6% it would be less attractive. Can you clarify a little further here?

Hi Todd,

In the example that I presented, I talked about multiple different bonds. One of these bonds had a yield of 3%, whereas most of the other bonds (that are similar) have higher yields (6%). As these other bonds have higher yields than the initial bond, the price of the initial bond will likely decline because it has a much less attractive yield than the 6% bonds.

Hopefully, this helps. If you have any follow-up questions, make sure to let me know.

Thank you for explaining this very complex and difficult to understand topic. I was in my 30s before I really understood what a bond was. I wish I had found your site years ago. You’ve added to my limited knowledge and I appreciate it.

Just last week I was trying to discuss the topic of bonds with my daughter and the various ways she could invest her savings for little to no risk. I failed in conveying the message successfully as she was more confused after our conversation lol. I am going to share your site with her. Thanks again!

Hi Shannon,

Thanks for sharing this. I truly hope that my post will help develop your daughter’s understanding of the bond market.

Hey Louis, I’m glad to have stumbled on your comprehensive guide on bonds, since I’m trying to learn what it’s all about. I’ve already experienced investing in stocks, mutual funds, and index fund in my country, since my family and friends are expecting me to get good at it so I can invest and grow their wealth for the long-term.

In short, I’m like their designated fund manager (lol)

Like you said, riskier bonds tend to have higher coupon rates while safer bonds don’t yield that much, which is the same trend I’ve noticed with mutual funds. If this is the case, why do you think should I give bonds a chance to be part of my investment portfolio? What is its advantage over mutual funds and index funds? Please enlighten me on this issue.

Hi Dominic,

Mutual funds are designated investment funds with many holdings, whereas bonds are standalone securities. So one advantage of investing yourself over investing in a mutual fund is that you have much more control. You can decide exactly where your money goes. Furthermore, you don’t have to pay any management fees as you are doing it yourself.

On the flip side, it certainly takes more time to trade/invest yourself.

Hello Louis,

A great & very informative article there. I was knowing something about shares but nothing about bonds. Reading this article now gave me more information about bonds than I had about shares. I understand that the investment is risk-free but wanted to know how to buy government bonds? Generally where to look for them? Where can I see these advertisements? Is the investment is tax-free?

Thanks for the in-depth information & I am going to share this page with my friends. Keep up the good work.

Chandrashekhar.

Hi Chandrashekhar,

First of all, I want to clarify that bonds aren’t risk-free investments. No investment is completely risk-free. The risk of Treasury bonds is just very low (but it isn’t zero).

Treasury bonds can be bought directly through a broker, a bank or directly from the US Treasury.

The interest earned from Treasury bonds is subject to federal income tax.