A very well-known and controversial market theory is the Efficient Market Hypothesis. It states that markets are efficient which means that all available information is always reflected in an asset’s price. The controversial implication of this would be that it is impossible to reliably beat the overall market because it isn’t possible to find any under or overvalued assets.

If this is true, it would make the act of actively analyzing and searching for potentially profitable trades pointless as there would be no way of acquiring an edge over anyone else. Instead, the best strategy would be a passive market-based investment strategy. So the big question is: Is the Efficient Market Hypothesis wrong or are we missing something?

In this article, I will discuss the question of efficient markets, its implications and the role of skill vs luck in trading.

The Idea Behind The Theory

Let’s start by briefly touching on the idea behind the Efficient Market Hypothesis. The Efficient Market Hypothesis states that markets are efficient and all available information is reflected in an asset’s price.

The idea is that if some information is not reflected in the price because it is new, limitedly known or due to some other reason, investors will act upon it and buy or sell the asset until the information is accurately reflected in the new price. This process happens on a constant basis and thus the price will always reflect all available information.

Information can take many forms such as news announcements, financial reports, rumors, expectations, or anything else that might be relevant for an asset’s value.

The goal of a winning trading strategy is to reliably exploit some kind of inefficiency to outperform the overall market. In an efficient market, however, there are by definition no inefficiencies to exploit. Therefore, it is hopeless to try to develop such a strategy in an efficient market.

Is The Market Efficient?

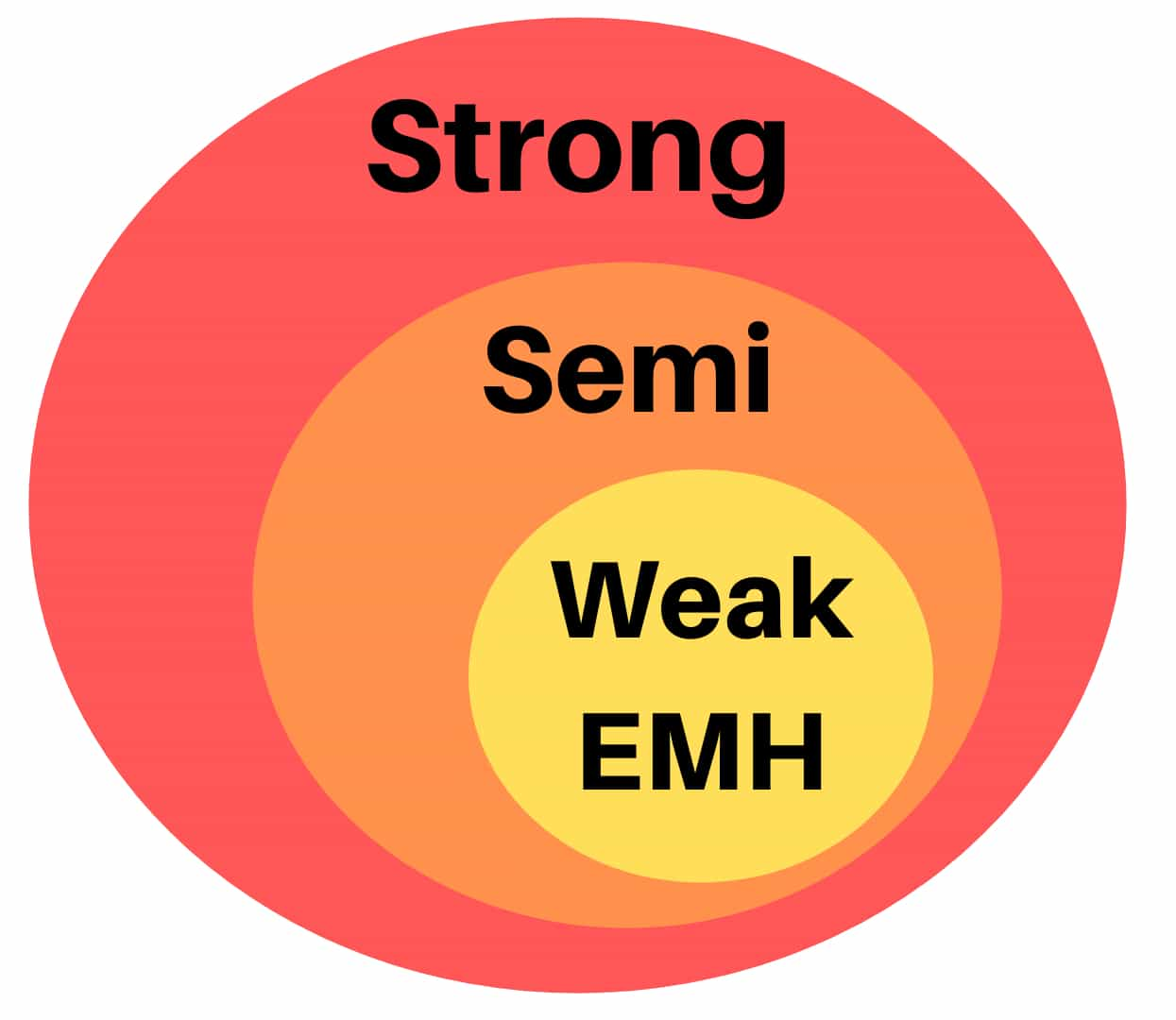

To answer this question, we must first ask ourselves, what does efficient even mean? The Efficient Market Hypothesis has multiple answers to this question. It defines different forms of market efficiency, ranging from weak to strong. So let’s first break down the different forms of market efficiencies.

Weak Form Market Efficiency

The Weak Efficient Market Hypothesis states that technical analysis is of no use, however, some forms of fundamental analysis can help determine if an asset is under or overvalued. This, however, is only possible over the short term because new information will be priced in correctly after some time. In other words, all past information is already reflected in the asset’s price and new fundamental information takes some time to be reflected correctly in the price.

Semi-Strong Form Market Efficiency

In the Semi-Strong Efficient Market Hypothesis neither technical nor fundamental analysis has any effect on your trading results. All publicly accessible information is already correctly reflected in the current price. Thus, only private, limitedly known information can lead to higher than average returns. New public information will be priced in without any delay.

Strong Form Market Efficiency

The Strong Efficient Market Hypothesis suggests that all available (both public and private) information is always reflected in the current price. So there is no information or anything else that will give you an edge. Therefore, it is impossible to reliably and consistently achieve a higher than average return.

Note that no form of the Efficient Market Hypothesis states that it is impossible to achieve a profit or even a higher than average profit on any trade. It just says that in the long run, it isn’t possible to consistently and reliably outperform the market.

With that being said, let’s try to answer if markets are efficient and if so, which form of the Efficient Market Hypothesis is the best representation of reality? Or if not, is the Efficient Market Hypothesis wrong?

To answer this question, let’s look at some of the arguments for and against efficient markets.

1. How Does Information Spread?

With the internet and its ever-increasing speed and ease of access, information can spread faster than ever. With newsletters and real-time notifications, it is even possible to act upon news within seconds of its release. Furthermore, most institutional trading firms use algorithms that allow them to automatically react to new information immediately upon its release.

Nevertheless, I’d say that information spreads in a progressive manner meaning that not everyone sees and acts upon it at the same time. Especially, among less liquid and lesser watched stocks, the delay between news and a reaction to it can be significant. Due to these delays and informational inefficiencies, I would say that new information is not immediately reflected in an asset’s price.

2. Is Trading Skill or Luck?

You might be asking yourself, why are there so many successful traders if the Efficient Market Hypothesis is true? Aren’t investors such as Warren Buffet living proof that the Efficient Market Hypothesis can’t be correct?

Proponents of the Efficient Market Hypothesis have a very simple explanation for outliers such as Warren Buffet. The explanation is: they just got lucky.

At first, this might seem like a very preposterous claim, but after putting some thought into it, it actually isn’t as absurd as you might think. In a population pool of millions of investors, some just ought to be successful by pure chance. Every distribution has its outliers, why should this differ here?

Let me present you with an example that clarifies all this.

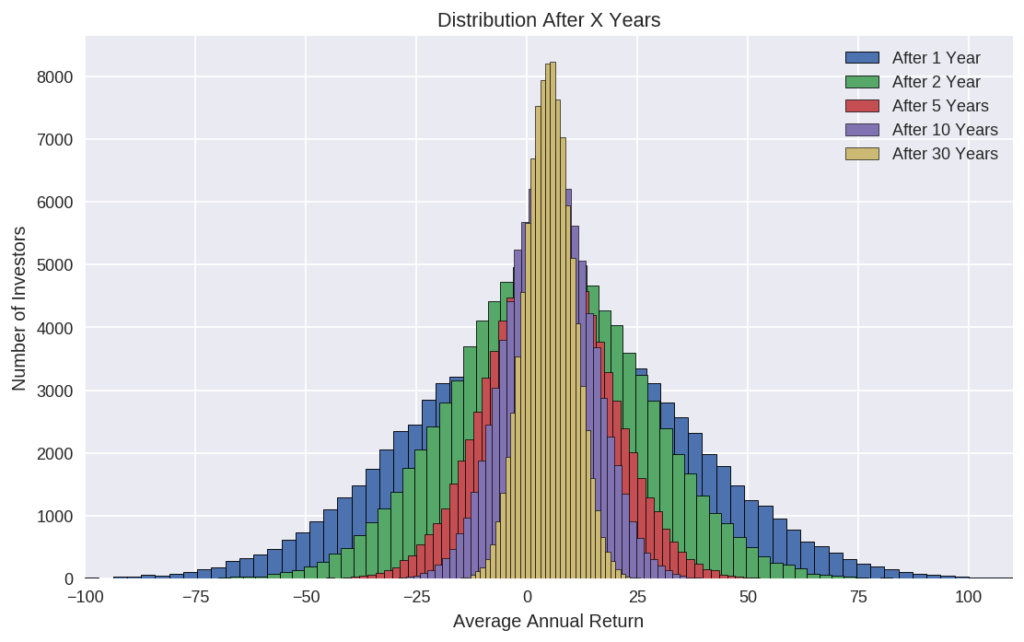

For our example, we will consider a group of 100’000 investors that are trying to achieve the highest possible return. In our example, skill plays absolutely no role in the likelihood of success for our investors. Instead, everything is based on luck.

We’ll say that on average an investor achieves an annual return of about 5% (for reference the S&P500 has an average annual return of about 10%). Furthermore, we will assume a normal distribution of the returns with a standard deviation of 30%. This means that about 68% of these 100’000 investors will achieve an annual return between -25% and 35% after one year.

The following graphic depicts the distribution of the average annual returns of these 100’000 investors after 1, 2, 5, 10, and 30 years.

The blue histogram all the way at the back describes the distribution of their returns after only one year. As you can see, most investors achieve a return of somewhere around 5%. However, due to the nature of this distribution, some investors will win big while others will lose big (over ±100%).

You can clearly see, the more time passes, the tighter the distribution becomes. It slowly moves to the mean return of 5%. Nevertheless, even after 10 years (the purple histogram), a handful of investors still achieve an average annualized return of 40%. Even after 30 years, some investors manage to significantly outperform the rest with an average annualized return of 25%.

So as you can see, depending on which distribution you choose, long term returns of Warren Buffet’s size are possible even in a completely efficient market.

With that being said, I am not claiming that this is how investor returns are distributed and markets are completely efficient. The purpose of this example is simply to show that it is entirely possible to outperform the market over the long run purely based on luck in a world were the Efficient Market Hypothesis is true.

What the just shown example does not account for is the lack of volatility and consistency of some investors. Most of the investors with very high average returns had big swings between their year to year performance. In reality, many of the very successful investors manage to achieve the same outstanding returns with amazing consistency.

3. Why Is The Efficient Market Hypothesis Wrong?

Besides the aforementioned points, there are many more arguments that speak against the Efficient Market Hypothesis. It is these points that I want to present next:

- Limited Liquidity: There are many less liquid and less-actively watched stocks. When new information about them is released, it often takes days before the stock reacts. Therefore, I find it highly unlikely that all available information is always correctly accounted for in their price.

- Human Irrationality: Humans aren’t completely rational beings. Many people base the majority of their decisions on emotions instead of principles of complete rationality and information. Often people don’t seek out information even if it is available. This can lead to entirely irrational valuations of assets and market bubbles. In my opinion, the Efficient Market Hypothesis does not account for the limited rationality of humans.

- Subjectivity: Besides irrationality, humans are also prone to subjectivity. Asset pricing and valuations aren’t only based on quantitative data that can be directly compared. Instead, many aspects of pricing require individual judgment. This means even with exactly the same information, different people often arrive at different valuations. This raises the question of what is the true price of an asset given all information?

- Market Bubbles: The Efficient Market Hypothesis fails to explain how market bubbles and crashes occur. If all information is always correctly accounted for, how can prices halve from one day to the next without a huge underlying economic turn? In a completely efficient market, this should not be possible.

- Too Many Counterexamples: Even though this doesn’t disprove the Efficient Market Hypothesis, I find it quite unlikely that there are so many people that manage to consistently outperform the market if it were completely efficient. Furthermore, an entire gigantic industry is based on the assumption that the Efficient Market Hypothesis isn’t true.

Conclusion – Are Financial Markets Efficient?

If the Efficient Market Hypothesis were true, stock selection and analysis of any kind would be rendered useless. Therefore, the best strategy in an efficient market would be a passive, index fund investing style.

But do I think that markets are efficient?

Due to the reasons stated above, I do not believe that markets are anywhere near as efficient as the Efficient Market Hypothesis states. In my opinion, the idea of 100% efficient markets is utopic. As long as there are human traders, there will be inefficiencies that can be exploited.

Nevertheless, it is important to note that through automation, advancements in technology and increasing trading volume, markets are becoming more and more efficient. This is likely one reason why the more passive approach of index fund investing has become increasingly popular over the past few years.

Already now, it is very hard for retail traders to take advantage and trade based on news announcements alone, especially among very liquid and actively watched stocks. It takes more than being early to consistently beat the market.

In conclusion, I am of the firm belief that it is still very much possible to develop a winning trading strategy that consistently outperforms the market based on skill and in-depth analysis.

If you liked this article, check out my in-depth analysis of the Random Walk Theory as well.

What do you think? Do you believe the Efficient Market Hypothesis is wrong? I’d love to read your thoughts in the comment section below!

I believe efficient market hypothesis has some truth to it, but can’t be absolute. Of course skill and insight will always play a role, because there are some things which just aren’t in your control. Take for example some natural disaster or a disease like corona, there will always be things you don’t have control over. That’s just the way the word works.

With regards to technology, having taken some computer science courses, made me realize that software and technology are nothing but a step-by-step plan/recipe made by a human.

Meaning that it will always be limited and have shortsightedness no matter, because the one who set it up was limited and shortsighted. Let alone other factors like hardware failure and so on…

Maybe things will become different, requiring new strategies, but I don’t believe that skill will ever die.

Thanks so much for sharing your thoughts about efficient markets. I certainly agree with you that skill will always play some role when it comes to trading and investing.

The question of whether the market(s) is (are) efficient is one that I discuss often with my fellow investors. At times it seems they are not, but in the long-term, I think they are. At times, the reaction to events that are taking place in the world can have a short-term effect, but the markets tend to correct this over time.

The efficient market hypothesis is one that has been around since well before I started investing 30 years ago, but it was one of the first tenets that I was taught by older investors when I was in my late 20’s. The factors that you mention against acceptance of the theory all do have an effect (i.e. human irrationality, subjectivity, and market bubbles)…

It is interesting that there is a segment of investors that manage to eke out a handsome profit year in and year out, no matter how the market may be acting, efficiently or not. The investing attributes and conditions they use to select their investments are the ones I like to follow. It has helped me a lot, and anything over the average return is okay with me. Good article, I will be back to read through this again, as you have put a lot of ideas into this and I am always open to other points of view. Thanks.

Hi Dave,

Thank you so much for your comment and thoughts on efficient markets. I am very glad to see that you enjoyed the post.

Thank you so much for sharing with us such a beautiful article. I am glad to see your article. I think that it’s fascinating and interesting. I accept the efficient market hypothesis has some fact to it, however, can’t be supreme. Obviously, expertise and knowledge will consistently assume a job, on the grounds that there are a few things that simply aren’t in your control. Perhaps things will get unique, requiring new techniques, however, I don’t accept that expertise will ever pass on. I am very happy I got the chance to read this and hope the best for you and your site in the future. I must say that this article is very amazing and informative. Thanks for sharing.Good Luck!

Thank you for commenting. It’s great to see that you like my content.