What does the stock market have in common with random movement? The Random Walk Theory says everything. According to the Random Walk Theory stock price changes happen in a so-called random walk. This means they are entirely random and therefore cannot be predicted in any way, shape, or form.

Due to its implications, this is a very controversial theory that has sparked a lot of debates, even among well-known economists and traders. Research studies exist that support both sides of the Random Walk Theory.

The aim of this article is to determine if there is some truth to the Random Walk Theory and if so, what does it mean for traders? The answers to these questions have some staggering consequences for the world of financial markets and traders of any kind.

The Random Walk Theory

Even though the concept behind the Random Walk Theory has existed since the 19th century, it has first become widely popular with the release of Burton Malkiel’s book “A Random Walk Down Wall Street” in 1973.

The theory states that asset prices move in a random walk. But what exactly is a random walk?

A random walk is a random sequence of discrete steps in a given mathematical space. Let me give you a concrete example to clarify this. A random walk could look like this: You flip a coin and if it lands on heads, you move a step forward and if it lands on tails, you move a step back. A random walk is possible in any dimension.

The most important characteristic of a random walk is that it is truly random. This means that every step is independent of the last one and thus, you can’t reliably predict the next step.

Let’s now apply the concept of a random walk to stock prices. The Random Walk Hypothesis describes stock price changes as one-dimensional random walks. This means, at every step, stock prices have a certain probability to either increase or decrease. This increase or decrease is influenced by nothing. It isn’t the result of past moves, news announcement or anything else. According to the Random Walk Theory, it is a completely independent random event.

More specifically, asset price changes are most commonly modeled as Gaussian random walks with a slight upward drift. A Gaussian random walk simply means that the size of the price changes follows a normal distribution. Furthermore, the upward drift means that the random walk has a slightly higher chance of going up than down. This slight upward drift is supposed to explain why the overall market has increased since its inception.

The just described conditions are also used in the Black Scholes options pricing model as well as in various other financial market models.

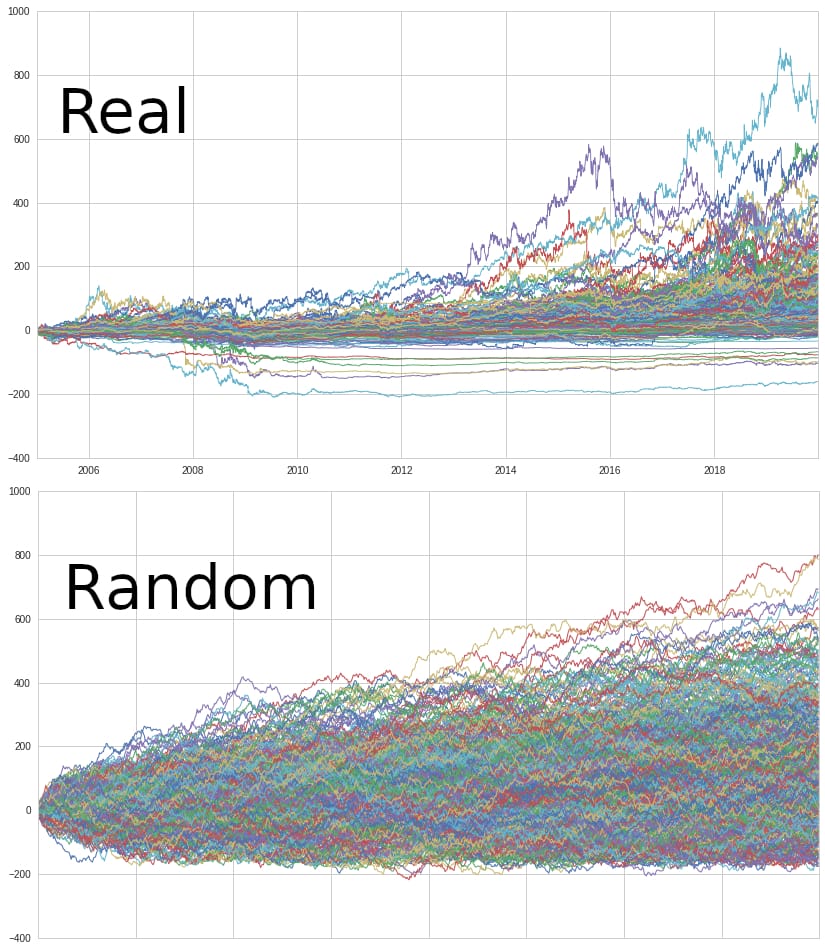

So far, you might find the notion that price changes are completely random a little weird. To convince you otherwise, let’s play a small game. Look at the following two plots and try to determine which of them is a real stock chart and which has been generated from random data.

Now let me reveal the answer: the green plot B is the price of TSLA from 2013-2015, whereas the blue plot A is random data generated according to the random walk model described above.

Did you guess that right? If so, was there anything that gave it away or was it just luck?

Objectively speaking, there is nothing that clearly distinguishes these two plots. They even seem to be somewhat correlated. I hope this brief example clarifies the resemblance of random data to asset prices.

Is The Stock Market Predictable?

As you now know what the Random Walk Theory entails, let us move on to its implications if it is true. Since every step in a random walk is independent of any other, past moves say nothing about future ones. Furthermore, every step is a random event, therefore, it cannot be predicted reliably. This means it is impossible to reliably predict any price changes.

Due to this, technical, fundamental, and any other form of stock analysis is utterly useless. There is no reliable way of picking or analyzing stocks that will give you an edge over anyone. No matter if you are a professional trader, investment advisor, analyst or anyone else, you have no way of reliably beating the market.

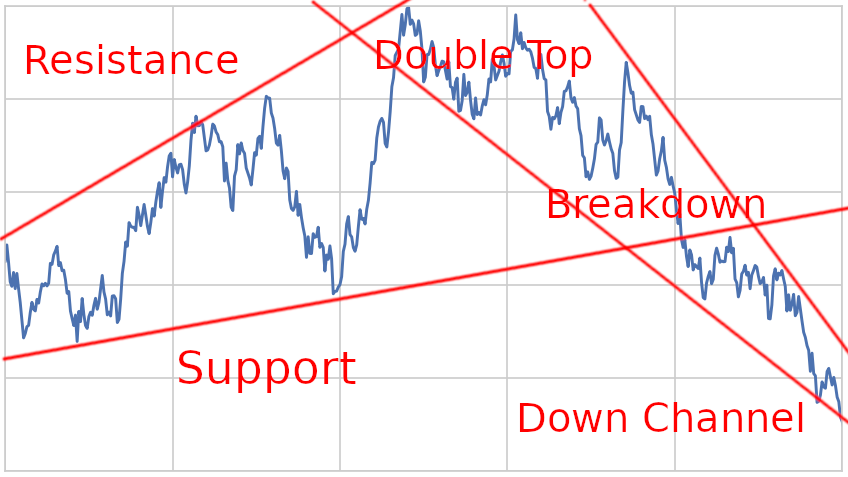

Just look at the following chart. The blue plot was, once again, created from completely randomly generated data.

It is very easy to spot and apply various different technical analysis tools to it. The chart had an obvious upward trend with clear support and resistance levels followed by a double top and a breakdown that has now turned into a downward channel. All of this sounds good, but it doesn’t make any sense because it is just random data and analyzing past patterns tells you absolutely nothing about the future behavior of this random data.

Proponents of the Random Walk Theory argue that it is just as pointless to apply technical analysis to real asset prices as they are just as random.

So what is the best strategy in a random market?

The random walk seems to have a slight upward drift which explains the market’s tendency to go up since its inception. But as stock prices are independent random events, stock selection doesn’t work. Thus, the best strategy in such a market would be passive, buy and hold index fund investing. Index funds have low fees and simply follow the overall market without trying to select the best possible assets.

Note that the Random Walk Theory does not claim that it is impossible to beat the market. It doesn’t even claim that you can’t outperform the market over the long run. It just says that you can’t reliably do so because if you do so, it is based on luck instead of skill. Therefore, the highly consistent returns of successful investors such as Warren Buffet aren’t enough to disprove the theory.

If you choose the right underlying distribution, return’s of investors such as Warren Buffet are possible in a purely random market. If you want to see a detailed example of this, I recommend checking out my article on the Efficient Market Hypothesis.

Speaking of the Efficient Market Hypothesis…

What is the difference between the Efficient Market Hypothesis and the Random Walk Theory?

Even though these two theories are similar and both claim that it isn’t possible to reliably outperform the market, there is a key difference in their view of the market. The Efficient Market Hypothesis states that all available information is always correctly reflected in the current price of an asset. Furthermore, new information will be priced in correctly without any delay.

The Random Walk Theory, however, says that prices follow a random walk. It does not claim that the current price is rational and reflects any information. This is an important distinction that many people aren’t aware of.

Is The Random Walk Hypothesis Wrong?

You should now be familiar with what the Random Walk Theory is and what consequences it entails. Even though you can’t directly disprove the theory, it is possible to show that it is unlikely. That’s what I’ll try to do next.

- Underlying Distribution: The most commonly used random walk model for stock prices assumes a normal distribution of stock price changes. This isn’t necessarily the best representation of reality since stock price changes often have far more outliers than they should according to a normal distribution. The two charts below show how the distribution should look according to the random walk described above and how they actually look. (Check out my article on the distribution of stock market returns to learn more about this topic.)

With that being said, it is theoretically also possible to model asset prices as a random walk with a different underlying distribution.

- Improbable Correlation: If asset prices behave according to a random walk. they should have low to no correlation to anything. A consistently high correlation would be a contradiction to the randomness. In reality, however, asset prices are often heavily correlated to each other, news events, and other factors. Furthermore, certain assets have an unlikely high degree of predictability over certain time frames.

- Insider Trading and Information Asymmetry: Insider trading is the act of trading public securities based on non-public information. This is considered exploiting an unfair advantage and thus, insider trading is illegal. There have been countless scandals in which managers or employees of certain companies have illegally earned great sums of money by exploiting private corporate information. If, however, asset prices moved on a purely random basis, this would make no sense. The same goes for the vast amounts of data that institutional investors use to try to achieve a profit.

- Simplification of Reality: The Random Walk Theory is often used to mathematically model asset price changes. Even though randomness has many similarities with the behavior of asset prices, a random walk is still an obvious simplification of reality. It is a relatively simple model that tries to explain a vastly complex system of millions of interacting agents. I wouldn’t say it does a bad job of modeling this system, but it certainly doesn’t do a perfect job. Like all models, it has its flaws and simplifications. Therefore, it shouldn’t always be taken at face value.

- An abundance of Outliers: Many investors manage to consistently significantly outperform the market over vast stretches of time. Even though it is possible that they all got lucky, it isn’t likely.

- Inefficiencies: It is naive to say that the market is 100% efficient and there are absolutely no inefficiencies that can be exploited. The existence of arbitrage opportunities throughout the history of the stock market is enough to show that markets have their inefficiencies.

- Lack of Liquidity: Especially in lower-priced, less watched and less liquid securities, prices don’t seem to follow a random walk. Certain price reactions to news announcements are simply too sharp and too consistent to be purely random. In very illiquid securities, individuals can directly affect the price with large enough orders. This is a direct cause and effect relationship and thus, not random.

- Human Psychology: On itself, the behavior of securities is not random at all. A surplus of buy orders drives the price up, whereas an excess of sell orders does the opposite. The randomness only comes into play when enough participants start expressing a wide variety of different opinions in the form of buy and sell orders. In my opinion, however, the behavior of people, especially in large groups, is not purely random. Instead, it can be predicted, at least to some extent. Certain patterns arise due to cognitive biases, emotions, and human psychology, in general.

None of the just-mentioned points directly disprove the theory. However, I hope it makes the Random Walk Hypothesis seem less likely than before.

There have been many data-driven, statistical studies that tried to test the hypothesis, but none of them could irrefutably prove or disprove it. I’d say one reason for this is that price changes have a remarkable similarity to a random walk. Furthermore, there are periods in which markets behave more randomly than in other periods. Therefore, the results of these studies often depend on the time frame chosen. Last but not least, it is very hard to indisputably prove that something is or isn’t random.

Conclusion and Takeaways

At the very least, the Random Walk Theory is interesting and thought-provoking. But in my opinion, it is more than that. It shouldn’t be dismissed completely as there is some truth to it. Asset prices do resemble randomness to some extent.

Do I think that asset price changes are completely random?

No, but especially in the short term, asset prices are very hard to predict and they sometimes seem to move as good as random. Therefore, I do think that luck does play a bigger role in successful trading than many people like to admit.

Many professional investors fail to consistently beat the market, even though they charge huge commissions for their know-how. The Random Walk Theory does shed some light on their inability to outperform the market.

It is often not possible to break everything down to a simple cause and effect relationship, even though financial professionals such as analysts and news organizations often try to do so.

One takeaway from the Random Walk Hypothesis and this article should be that passive buy and hold investing is a very good and often overlooked strategy. It is often better to simply buy and hold a well-diversified portfolio of value stocks and index funds than to pay high commissions to active-fund managers for their ‘great insights’. Statistically speaking, most fund managers fail to outperform the market, especially when commissions are factored in.

With that being said, the Random Walk Theory is still a too big simplification of real-world conditions. Nevertheless, the Random Walk Theory is not a bad approach to modeling asset price behavior. But the theory and its implications shouldn’t be taken as a fact since markets are a very complex system that cannot easily be described by such a model.

I’d say it is very much possible to beat the market even with a non-passive buy and hold strategy. But it is important to note that it is quite hard to consistently do so.

Check out “The Random Walk Down Wall Street” on Amazon.

I hope you enjoyed this post on the Random Walk Theory. What are your thoughts on this theory?

I have to admit, that reading your article made me realize just how little I know about the stock market. Enjoyed reading about the random walk theory, and would definitely like to do some further research into it. My husband and I both have a 401K we invest in. His is a federal TSP, where he has joined a group that follows algorithms on when to make changes/moves with shares to increase earnings. So far, it has been doing really well (minus the crash we just experienced with the coronavirus and oil wars). What are your thoughts on following an algorithm for moving shares?

Hi Brandy,

Thanks for your comment. I’d say algorithmic trading is just as good as a discretionary approach. Over the past decade, the role of algorithms in trading has grown tremendously. I believe this trend will continue more and more.

You could also check out my article on algorithmic trading for a more detailed answer.

The random walk theory is a very interesting read. I have heard of it many years ago but I never knew just what it was till I read your article. Great way to explain it.If you look at the stock market while it does seem random at times there is also a somewhat predictable pattern it seems,so not random. This latest bear market though caused by oil and also coronavirus it was due. Historically about every ten years.

I think there’s some truth to the random walk theory, but I think it’s more of a combination of several factors, with the random walk theory being just one of the factors. For me, policy making, actions of central banks, foreign policy, and trade are all factors that direct the market – but the random walk is another factor in doing so. I think the market is predictable, but also unpredictable, and has a lot to do with mentality of the investors in buying and selling, which in turn justifies the random walk theory playing into markets.

I can usually predict a rise or fall in the markets by taking note of the factors I listed above, but at the same time the market may do the exact opposite of logic – hence random walk. It can be a chess game at times.

Hi Todd,

That’s a great comment. Thank you for sharing your thoughts. I certainly agree that the factors you mentioned have an effect on the market and its direction.