The goal of a trader is to best possibly position him/herself to maximize their chances of winning. To do this, it is crucial that you as a trader understand the underlying probability distributions of stock market returns. Without having a good understanding of price distributions, you might base your entire trading approach on completely flawed assumptions. This can have detrimental consequences and is one reason for financial crashes and crises.

The purpose of this article is to give you a broad overview of different distributions used to model equity markets and to show you the destructive consequences of being unaware of them. This will hopefully help you gain a better understanding of the stock market and show you certain statistical tools that can be used to model it.

Are Stock Returns Distributed Normally?

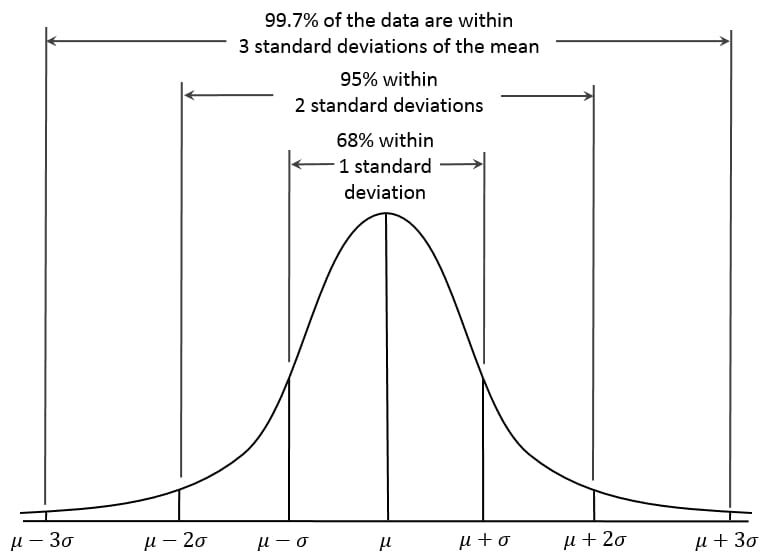

By far the most commonly used distribution is the normal distribution. If you ever had any kind of statistic classes, you will have heard of it. But just to make sure, let me briefly break down the normal distribution for you.

The following diagram shows a normal (gaussian) distribution where μ is its mean and σ is its standard deviation.

As you can see, a normal distribution has a bell shape and the vast majority of occurrences fall somewhere around the mean. The further out you go, the fewer occurrences appear. Depending on the mean and standard deviation, the shape and position of the bell curve can vary. Human height is a great example of a normally distributed statistic.

Let us now apply the normal distribution to stock price returns. For all of the following histograms, I used daily return data from 2005 to 2020. Note that we will be focussing on shorter-term (daily) data in this article. The distribution for longer time periods such as monthly and yearly returns can look quite differently (more skewed and more normal). But in my opinion, the return distribution for shorter time spans is a lot more significant for retail and institutional traders alike.

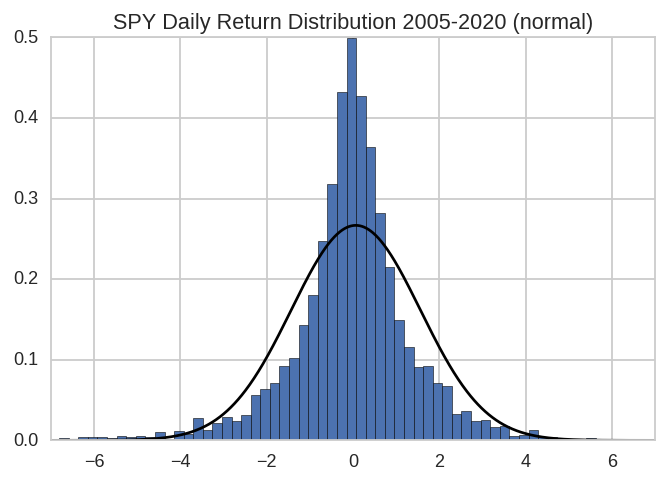

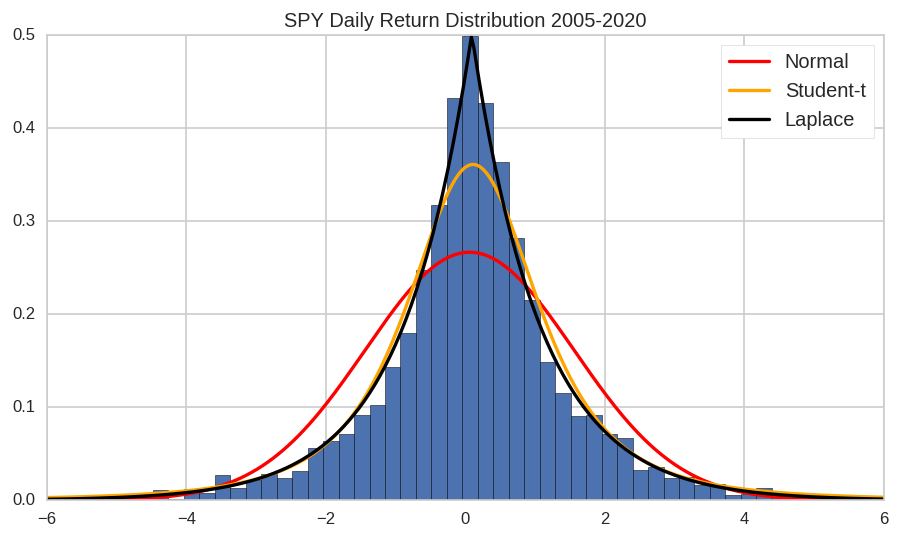

This first histogram depicts SPY’s daily returns (SPY is an ETF tracking the S&P500 index). The black plot has the shape of a normal distribution with the same parameters (mean and standard deviation) as the SPY data.

As you can see, the distribution has some sort of bell-like shape, but it is far from a perfect normal distribution! There are way too many occurrences right around the mean which is about 0. Furthermore, there are too few occurrences a little further out and too many all the way at the ends of both sides. This pattern repeats itself when you apply the normal distribution to other equities.

This does make sense as stock prices mostly tend to only move a little bit at a time. However, once in a while they move very far in a very short time span. But they don’t move moderately far at once too often.

This means that a normal distribution dramatically understates the probability of small and very big moves, whereas it overestimates the likelihood of moderately sized moves.

Especially the underestimation of big moves can be problematic in financial market models. For instance, market crashes such as the one in 2008 or 2020 are extremely unlikely according to a normal distribution. By extremely unlikely, I mean ‘once in a million + years’ unlikely! No wonder that market crashes seem so unforeseeable when such models are used to assign probability values to them.

By now, it should be clear that a normal distribution is not exactly a great model for stock returns. Nevertheless, it is the most popular choice of distribution to do exactly that. For instance, the Black Scholes Model assumes a normal distribution of stock returns. But if a normal distribution clearly doesn’t do a great job, why would you choose it over another, more accurate distribution?

The normal distribution is (one of) the most-researched and best-understood probability distributions in statistics. Therefore, it is very easy to work with a normal distribution. Certain mathematical models and tools would simply not work with other distributions. That’s why a normal distribution is often preferred over other ones.

A More Accurate Probability Distribution of Stock Market Returns

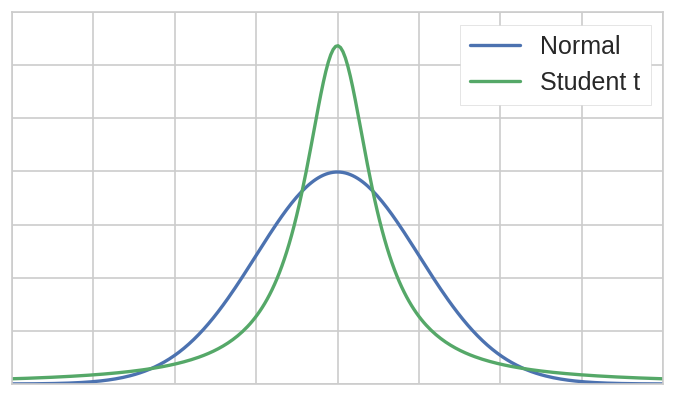

With the normal distribution out of the way, let us find a distribution that better resembles the actual shape of equity returns. What we need is a distribution that is taller at the mean and that has fatter tails. One distribution that does exactly that is the student t distribution.

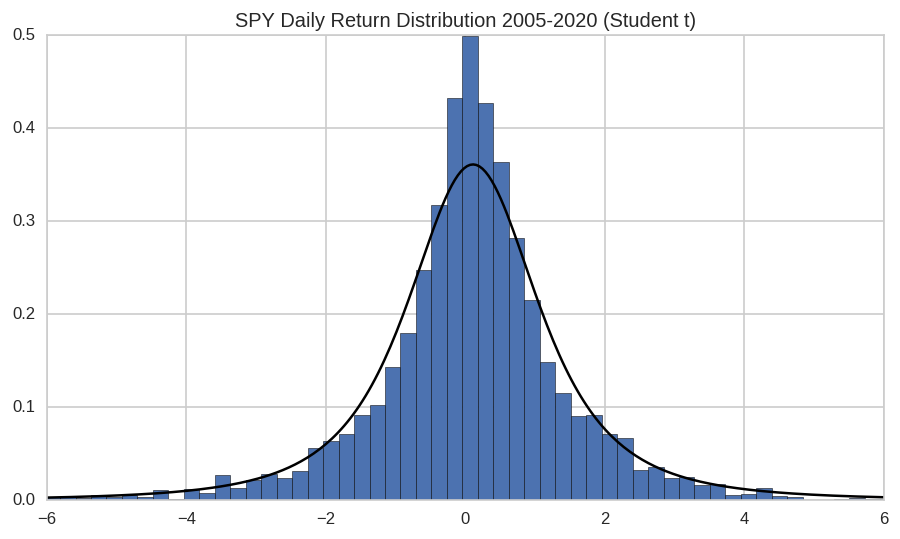

If we apply the student t distribution to our SPY dataset, it does a better job than the normal distribution, especially at the extremes. This is already a significant improvement because the underestimation of big moves in the normal distribution can lead to grossly flawed risk assessments in certain models. Nevertheless, the student t distribution still understates the number of occurrences of smaller moves.

The student t distribution is already a definite improvement over the normal distribution. But I think we can find an even better distribution, namely the double exponential or Laplace distribution. It is a symmetrical distribution with fat tails and a tall peak right at the mean – exactly what we want. Here is a diagram with the normal, student t, and double exponential distribution fitted to the SPY daily return data:

It is clearly visible that the Laplace distribution does the best job in approximating the actual distribution of SPY’s returns.

Even though a quick visual comparison is a good benchmark, it is important to test the fit of different distributions through rigorous statistical tests. If you are interested in seeing the results of such tests, you could check out this research paper as well as Eugene Fama’s article on the behavior of stock prices.

What is the Right Distribution?

Even though the Laplace distribution does a good job of describing SPY’s returns, it is by no means clear that the Laplace distribution is the best choice of distribution to model all equity returns. But it seems to be a much better choice than the normal distribution. Let me now sum up some of the key characteristics of stock return distributions:

- Symmetry: Equity returns don’t seem to be asymmetric. Their average return is mostly positive, but around this mean, there isn’t a clear tilt in any direction. Statistically speaking, there haven’t been significantly more or fewer (big) moves in either direction from the mean.

- Fat Tails: One striking trait of the probability distribution of stocks is its fat tails. Extreme moves occur much more frequently than they should according to a normal distribution. These ‘outliers’ should definitely be accounted for in the chosen distribution to accurately model risk.

- Tall Peak: The vast majority of daily stock price changes fall right around the mean.

Besides the Laplace and student t distribution, there are many other distributions that fulfill these requirements. Another good choice, for instance, would be a Pareto (power-law) distribution. But sadly, a normal distribution does not have all these characteristics, therefore, it isn’t a very accurate model for equity returns.

Why This is Important For You!

So far, we have gone through an array of different distributions and their resemblance to the distribution of stock market returns. We have come to the conclusion that there are far better choices than the normal distribution. But what does that actually mean for traders such as you and me? That’s what I’ll present next.

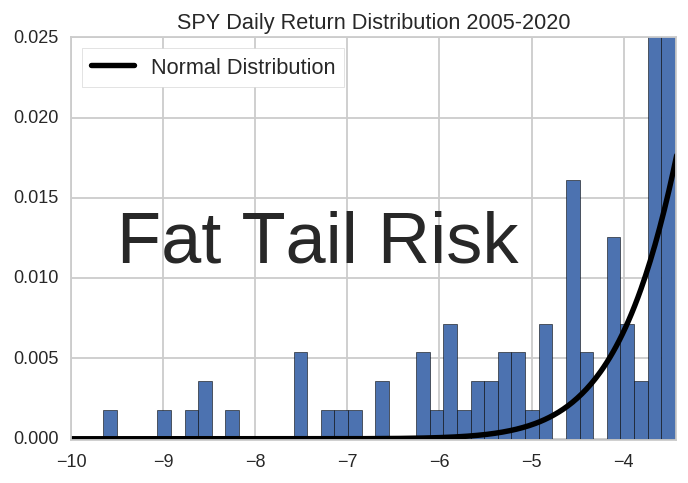

Fat Tail Risk

Let’s start with the very important concept of fat tail risk (also known as kurtosis risk). Fat tail risk is the risk that arises when you assume a normal distribution on an observation that, in reality, has much fatter tails than a normal distribution. In other words, it is the risk that arises from systematically underestimating the likelihood of large deviations from the mean (typically to the downside).

The following image is a zoomed-in version of the diagram above. It shows the left tail of the SPY daily return distribution. The black line is a normal distribution fitted to the data.

As you clearly can see, the normal distribution dramatically understates the chances of these large down moves. The same is the case for large up moves, but these usually don’t cause as much harm as big price drops.

It is still common practice to use a normal distribution to model equity prices. For instance, Markowitz’s Modern Portfolio Theory or the Black Scholes Model both assume that stock price returns are normally distributed. That’s why many institutions and portfolios usually aren’t prepared for these huge price drops.

Don’t get me wrong, these huge price swings are rare, but not nearly as rare as the normal distribution claims. Even though human cognition has a hard time differentiating between 0.01% and 0.0000001%, the former is 100’000 times more probable than the latter. This difference is a pretty big deal! Imagine the harm that can be done by underestimating your risk by a factor of 100’000!

These dramatic misjudgments of risk are one contributing factor to market crashes, crises, and blow-ups.

So how can you protect yourself?

Being aware of fat tail risk is the first step in the right direction. Here are two concrete strategies that can be used to decrease the fat tail risk in your portfolio:

- Hedging: The first and most obvious strategy is to simply have a hedge in place against big downward moves. This might seem unnecessary and expensive in the short term, but in the long run, it will protect you against any sudden drops. There are multiple ways of hedging your positions. If you want to learn more about this, you could check out my post on hedging strategies in which I break down two approaches to use options for portfolio protection.

- Diversification: Another great way to decrease fat tail risk is by building up a well-diversified, uncorrelated portfolio. It is less likely that all of your positions will suffer heavy losses at once than a single position at any given time.

A perfect example of the disregard of fat tail risk is the hedge fund management firm Long Term Capital Management. The firm was founded in 1984 and had a few outstanding years. Furthermore, it had multiple world-famous economists such as Myron Scholes and Robert Merton on its board (the creators of the Black Scholes Model). Nevertheless, the firm lost close to $5 billion in 1988 in the aftermath of the Asian and Russian financial crises because it dramatically underestimated the likelihood of such big price drops.

A great book on the topic of fat tail risk is former options trader Nassim Taleb’s “Black Swan: The Impact of the Highly Improbable”.

Check it out on Amazon

Besides fat tail risk, other consequences of assuming the wrong distribution include:

- Mispricing and mismodeling securities: If you assume the wrong behavior of an asset, you will likely also price it incorrectly. A great example of this is far Out of The Money options. According to a normal distribution, far OTM options have almost no chance of expiring In The Money, but in reality, they often do. Therefore, far OTM options are often priced too low.

- Overestimating the likelihood of moderately sized moves: Due to the relatively flat bell shape, the number of occurrences of moderately sized moves is greatly overstated. This can also be seen in options’ prices.

It is certainly possible to build entire trading strategies around these inefficiencies.

Conclusion and Takeaways

Many market theories fail because the underlying math is a too big simplification of real-world conditions. Assuming a normal distribution of stock returns is just another example of such a simplification. This simplification makes a lot of the math and the accompanying models easy to work with. Nevertheless, using flawed models can have detrimental consequences.

It is important for you as a trader to be aware of these consequences. For instance, always keep fat tail risk in mind when building a portfolio. Furthermore, if you develop your own trading algorithms and models, try to use a distribution that accounts for the aforementioned characteristics. Don’t be lazy and use the normal distribution.

I highly recommend checking out Nassim Taleb’s book “Black Swan”. The book is a must-read for traders of any kind and covers topics such as uncertainty, luck, human error, risk, probability, decision-making, and more.

Check Out The “Black Swan: The Impact of the Highly Improbable” on Amazon

Hi,

Thank you immensely for this very interesting and informative read into options trading. Your explanations on the probability distribution of stock market returns are written with great authority and knowledge on the subject which is very comforting indeed given the great swings in environments and circumstances as current circumstances portray the very factors that you advice must be taken cognizance of. The black swan of Covid 19 shows how your advised mitigation of risk strategies such a hedging and diversification as you say rightly may appear to be expensive at the time only prove very prudent to cushion the impact of such sudden moves even with the right probability models at inception. Thank you very much indeed for this very useful explanation and advice to read widely on the subject as in your recommended reading of Nassim Taleb;s book ‘The Black Swan’ to get more of an understanding of the possibility of these outsized moves.

Rami

Hi Rami,

Thank you for your comment and feedback. It is greatly appreciated.

Very interesting and informative aricle. Thanks

My pleasure

Very interesting and helpful article. Thank you!

You are very welcome!

Louis, thank you for a well written article. Not only do I appreciate the information you share, the way in which you present it is brilliant.

Johan

Hi Johan,

Thank you very much for the positive feedback!

finding a good article does not come by easily so i must commend your effort in creating such a beautiful website and bringing up an article to help others with good information like this. i had to read the entire page again to fully understand the implications of assuming the wrong distribution of stocks, but this is a good one

Hi Benny,

Thanks so much for your positive comment. It is greatly appreciated.

I really admire the business of trading. It seems so exciting as I watch it on CNN. Trading seems to have it’s language all its own and must take a whole lot of time to completely understand how it all works. Just going through this post is so intriguing because I can only imagine what this all means to traders all over the world especially during this challenging and changing time.

Hi,

If you are struggling with some of the terminology, I highly recommend checking out my free trading glossary.

Hi Louis, I would also include Benoit Mandelbrot’s “The Misbehavior of Markets” as recommended reading. He touches on a lot of the points you make and applies it to fractal math. His idea was that markets can go from mild to wild. Where in mild mode, markets do move in a normal distribution. But in wild mode things do not.

I am quite amazed that new options traders are still told that markets move in normal distribution. I bet if you expanded your dates for 100 years of market moves you find the same distribution. It would also be interesting to see the same by decade.

Hi James,

Thank you very much for the comment. I haven’t yet read “The Misbehavior of Markets” but it has been on my book-list for awhile now. I will definitely give it a read!

These probability distributions were taught in 1950’s, 60’s, and 70’s and continue till today. They spent many years using the Markov for speech recognitions, but finally gave up. The results of most of the probability distributions were presented in graphs and so on. They were convenient to use.

In my opinion with the software for artificial intelligence (AI), the days of classical probability distribution are over. One needs to embrace the results which are generated with AI software and make their decisions.