In this article series, I explain options trading examples:

This options trading example is a little different from all the previous trade examples. The main difference is the strategy, as this example isn’t a standard credit spread. This live trade example will cover an options butterfly strategy that I traded on SPY. If you don’t know what a butterfly spread is, I recommend to read THIS ARTICLE, as it fully covers what butterfly spreads are and how they work.

Before I begin, I want to let you know that all the example trades posted on this site, including this one are made from a separate, very small Tastyworks trading account ($1500-$2000). I do this on the one side because I want to show that it is totally possible to begin to trade with such a small account. Additionally, I can give you things to look out for when trading in small accounts.

Recently my trading in this account had some flaws and therefore I decided to change things up a little. This is also the reason why my setup is a little different than it usually is. To read how I adjusted my entire strategy to be better for smaller trading accounts, click HERE.

General:

The selection of an underlying to trade was pretty straightforward and very similar to the way I usually choose underlying securities to trade. In this small account, diversification isn’t as important as in bigger accounts. I actually didn’t even have any positions open before I opened this new trade. Therefore, I didn’t have to pay attention to my ‘portfolio’ at all. The underlying asset that I chose to trade my options strategy on was SPY, an ETF tracking the S&P 500. This is an extremely liquid asset with many millions of shares traded every day and with very high options volume as well. If I don’t have an existing portfolio restricting me, I often choose SPY as an underlying to trade.

Additionally, SPY’s implied volatility was relatively low. I could see this with the help of IV Rank. IV Rank compares the current implied volatility state of an asset to historical figures of the same asset. An IV Rank of 20 means that implied volatility has been lower than it currently is 20% of the times before. Generally, an IV Rank below 50 symbolizes a low IV environment and an IV Rank over 50 means that IV currently is relatively high. The IV Rank of SPY when opening my positions was around 10, which is quite low. Short butterfly spreads usually profit from a rise in IV, thus the low IV environment is very good for this strategy.

Strategy:

As I already mentioned, my strategy for this trade was a Short Butterfly Spread. This is actually a quite new strategy for me as I only seldom have traded it before. One reason why I chose to trade this strategy was that I wanted to try something new. Before, I mainly traded credit spreads in this account. But these weren’t working out that great in the past few weeks. Therefore, I wanted to try some other strategies in this account.

Furthermore, short butterfly spreads could profit much more from the low IV environment than strategies like credit spreads. Additionally, my credit spreads often ended in losses due to SPY constant rise in prices. SPY had quite a big run in the past few weeks. A short butterfly spread would also profit from a continuation of this run. But this only was a minor reason for my strategy choice.

Strategy Setup:

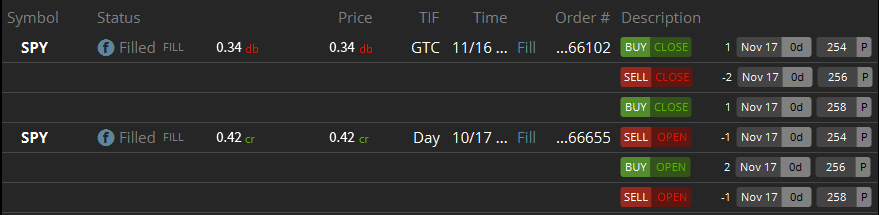

SPY was trading at ca. $255.5 at time of entry. I chose the following strikes for my short butterfly spread:

- 1 Long 254 Put

- 2 Short 256 Puts

- 1 Long 258 Put

The reason why I chose to do a put butterfly spread instead of a call butterfly spread was that it had better pricing and a higher probability of profit (POP) and frankly, this wouldn’t have made a real difference anyway, as both of these strategies are quite similar.

The selection of these particular strikes was more or less due to the same reasons (better pricing, higher POP).

Overall my probability of profit when opening my positions was 84%, which is very high. My maximum achievable profit and the credit taken in was $42. The maximum loss, on the other hand, was $158. I opened the spread around 30 days before expiration.

This is a larger position size than I usually have. This has multiple reasons. Initially, I had the strict rule to never allocate more than 5% of my portfolio for one single trade. But through testing, I found out that this rule isn’t suitable for very small trading accounts like this one. 5% just is too little to make trading worthwhile in such small accounts. Therefore, I’d rather only have very few positions open at once but with more allocation. The 5% rule still is good for bigger accounts.

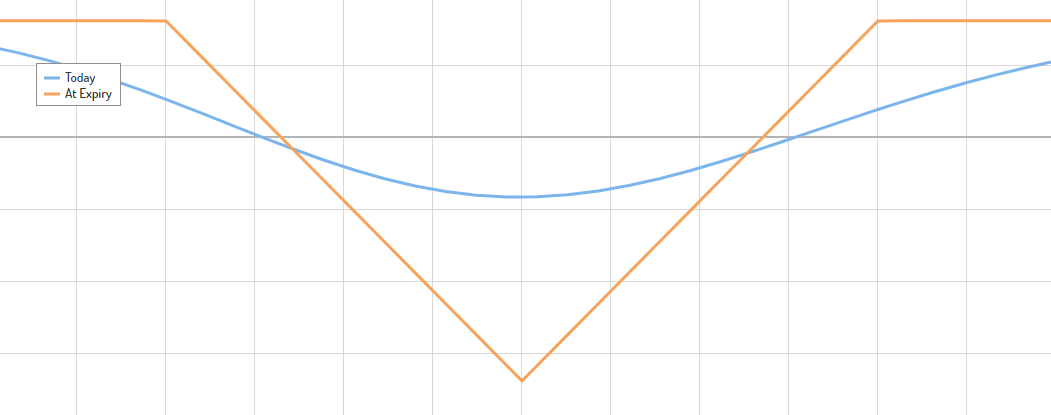

Additionally, as you can see on the payoff diagram of short butterfly spreads on the right-hand side, the max loss only occurs if the price is exactly at the strike price of the long options. The chances of this happening are quite low and thus the true allocation is probably a little lower than the $158.

Max profit occurs if the price of the underlying moves beyond one of the short puts and the spread will end with a loss if the price only moves very little. The breakeven points are between the short and the long puts. They are normally closer to the short puts than to the long puts.

The risk/reward ratio may seem like a bad one. But the probability of profit compensates that. To find out if this compensation is good enough, I do this calculation before every trade:

POP x Max Profit – (100-POP) x Max Loss

If this calculation is greater than zero, the price is good enough for me. Otherwise, I either adjust the price or don’t make the trade. This was the calculation for this short butterfly spread:

84 x 42 – 16 x 158 = 1000

The result of that calculation is clearly well above zero and thus the pricing is good in my eyes.

How the trade went:

Not too long after my order got executed, I sent out a GTC (Good-Til-Cancel) Order at around 65% of my max profit.

In the beginning, everything went just as planned, SPY’s price continued rising. Actually, everything went fine until the last few days before expiration. The prices had some up and down swings, but they still continued to rise. But the price was more volatile and was increasing at a slower rate than it had done before. IV Rank increased to 34, which my butterfly spread happily profited from. My probability of profit still stayed quite high and the butterfly spread was at 50% of max profit.

There were ca. 3 days left until expiration and the only thing that could create a loss in the credit spread would have been an unlikely big drop in prices. Guess what happened…?

A quite unlikely gap down, right into the not profitable range. IV Rank increased up to 59, which is the highest in a while. This move happened 2 days before the expiration date. My butterfly spread had a paper loss of $25 instead of a paper gain of $25. The drop-down continued until the market close. Luckily, the price bounced right back up on the next trading day. I closed the butterfly spread when it popped back into the profitable range. The profit was laughable $8 (minus $4 commissions). But I’d take that over a loss of $25.

After closing the positions, the price continued to rise a little further and in hindsight, I thought that I could and should probably have holden on to the spread for a little longer. But not much later the price fell back down into the losing range again. My exit was actually timed quite good.

The two circles on the chart below indicate entry and exit point. The two blue lines are the strikes of the short puts and they also give you a rough indication of the profitable range of this spread.

Conclusion:

In hindsight, I surely should have closed the spread at 50% of max profit. But it is always easy to say that afterwards. Usually, I always close my positions at around 50% of max profit and this trade really shows me why. Nevertheless, I couldn’t really have seen this drop coming, my probability of profit was high and everything was going well leading up to the ‘big’ drop.

But it does definitely make sense to close positions that aren’t far ITM in the week of expiration.

The spread captured and profited from the rise in IV. The increased volatility is quite interesting as it is quite a long time since volatility has been this ‘high’ in SPY.

I will definitely trade more short butterfly spreads in the future, as it really seems like a great strategy, especially for this account and in lower IV environments.

Check Out My Tastyworks Review!

Thank you for a nice look at the butterfly as applied to the SPY. I was wondering your thoughts on this strategy being used during earnings season. I know that the SPY is an index and therefore does not have earnings, but many companies have their earnings near the same time. Do you use this strategy during particular times? Or does it merely depend on whether your buying or selling the spread?

Hey Neil, great question!

Short butterflies may seem like a good strategy for events like earnings as prices tend to move a lot during these events. Nevertheless, I wouldn’t use a short butterfly to trade the actual earnings event. The reason for that being that implied volatility often drops exponentially on earnings and short butterfly spreads profit from a rise and not a drop in IV. But short butterfly spreads may be a good strategy to use in the past few weeks before earnings as implied volatility increases during those times and prices move much more.

I have never tried this strategy before. But it seems viable. I will probably test it out in the future. So stay tuned for an upcoming article!

This is a great example of taking diversified option trading because when you do it yourself and then at the same time show others how to do it as an excellent opportunity to make brands of value so that we can all be on the same page together. I look forward to more that are exactly like this

Glad to hear that you like it.

Louis,

I just like the way how to teach the strategies, much better than many others that I have gone thru. Keep it up!

Thanks a lot for the positive feedback! I really appreciate it.