When people hear of undefined vs defined risk option strategies most people just think of limited vs unlimited risk and nothing more. In this comparison, most people think a limited risk trade is an obvious choice. But actually, there are many more factors that should impact that decision. Sadly, most people don’t know these factors. In this article, I will break down all the differences between undefined and defined risk option strategies.

To visualize the differences in the best possible way, I will present them with an example. To keep things simple, I chose two simple option strategies to represent undefined risk and defined risk trades. The strategies are a bear call credit spread (defined risk) and a naked (short) call (undefined risk). The only difference between these two strategies is that the credit spread has a long call a few strikes above the short call. This added long call acts as protection and defines/caps the risk.

Just because I use these two strategies to explain the differences, does not mean that the differences only apply to these strategies. The differences can also be seen in most other strategies.

All the screenshots and the video below originate from Tastyworks’ broker platform. If you are interested in learning more about Tastyworks, you can read my full Tastyworks review!

Video Lesson

The video below covers the same topic as the article. I recommend watching the video and reading the article.

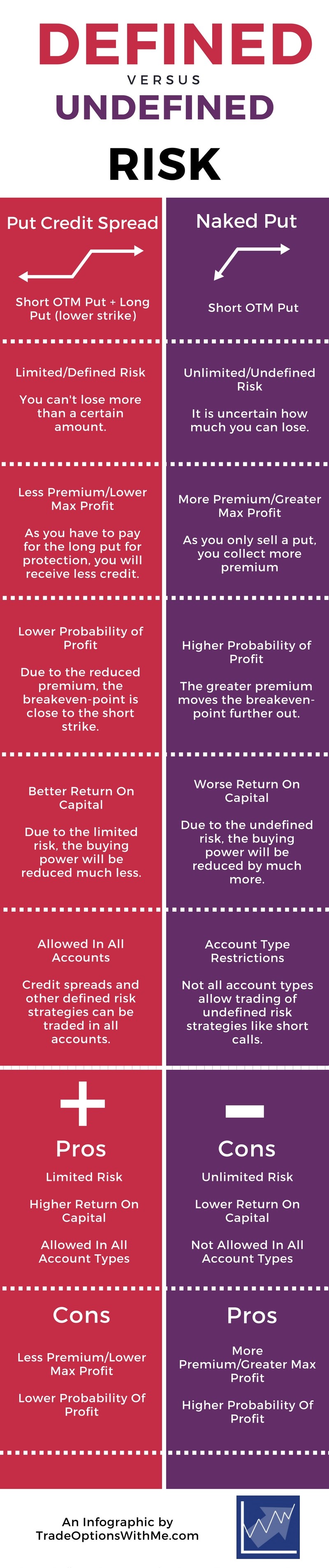

Comparing Undefined And Defined Risk Option Strategies

Options Trading Risk

Let’s start with the most obvious difference, the risk. Just like the name implies, defined risk strategies have a limited risk. There is only a certain amount that you can lose no matter what happens. This is very different for undefined risk trades as the risk is unlimited. When entering these strategies, you do not know your max possible loss beforehand.

Let’s say, you sold a naked call on SPY. At the time of the entry, SPY was trading at $275 and you chose the strike $280. This means you would reach max profit if SPY’s price is below $280 at expiration. But if SPY’s price rallies up and beyond $280 until expiration, you would end with a loss. The further the price goes up, the bigger this loss becomes. As there theoretically is no limit of how high SPY’s price can go, your loss can become very large.

Let’s look at the same scenario with one difference. This time, you opened a call credit spread. You sold the $280 call and bought another call at the $283 strike. Once again, SPY’s price rises sharply. But as soon as the stock price passes the $283 mark, your maximum achievable loss is reached (on expiration). From that point on, it really does not matter how much further the price would rise as your loss wouldn’t increase. This is the case because the profit achieved from the long call offsets parts of the loss achieved from the short call. So your loss at expiration if SPY would close at $350 wouldn’t be more than if SPY would close at $284.

This is the most well known and most obvious difference. But there are more differences that are important as well.

Premium – Max Profit

The next, still very important difference comes from the premium taken in. The premium/credit received when opening trades will almost always be larger for undefined risk strategies. This is because you have to pay for protection on defined risk strategies. This reduces the overall credit taken in.

Let’s take the example from before again. SPY is trading at $275 and you sell the $280 call for a credit of $2.63 or $263. These $263 are also the maximum achievable profit for that trade.

Now let’s compare that to the max profit of a call credit spread on SPY. You sell the exact same option for the same price ($283). Furthermore, you buy the $107 call for a debit of $1.63 or $163. In other words, you pay $163 for the added protection and therefore, your max profit decreases to $100 ($263-$163).

Together with the risk, the reward also decreases for defined risk trades. This can have more impact than you think. The next difference is a direct consequence of this.

Break-Even-Points – Probability of Profit

The decreased premium has an impact on the break-even-points and probability of profit (POP). More premium leaves more room for the price to move in before having a loss. In other words, premium creates a buffer room and moves the break-even-points further out. That is also why the break-even-point on a naked call isn’t right at the call’s strike price but somewhat further out. The greater this premium is, the further out this break-even-point moves out. This impacts the probability of profit. If the price of the underlying has to move further to create a loss in your position, the probability of profit increases as a big move is less likely than a small move.

Therefore the naked call from before has a higher probability of profit than the call credit spread. As you can see on the images, the credit spread has a probability of profit of 63% and the break-even-point is right at $281. The short call, on the other hand, has a probability of profit of 67% and the break-even-point is around $282.5.

Buying Power – Return On Capital (ROC)

A further major difference between these strategies is the impact on the buying power. Defined risk strategies have a limited risk and therefore, your broker only reduces your buying power by the amount of the risk. The buying power reduction for undefined risk strategies, however, is much greater as there is no real max loss.

Due to this, your return on capital (ROC) is much lower for undefined risk trades. You have to allocate more money to make a little more. Once again, I will explain this further with the example from before.

The max loss of the call credit spread on SPY is $200 ($3 x 100 – $100). This means your buying power will be reduced by $200 when opening this spread. In other words, you are allocating $200 to make $100. This is a return on capital of a 50%.

For a naked call, your max risk is theoretically unlimited. But obviously, your broker can’t reduce your buying power infinitely. Therefore, your broker assesses this risk and calculates the max loss of what they expect to be the max possible move in the underlying against you. Let’s say this is about $2700, so your buying power will be reduced by $2700. This means you are allocating $2700 to make $263. Now your ROC only is a little under 9%. The question to ask here is if it is worth it to allocate so much more money just to make $163 more.

This is especially relevant for traders that use most of their capital at once.

Account Type Restrictions

Not all account types allow you to open undefined risk positions. If you have an IRA (account), you won’t be able to sell naked calls, puts or other similar undefined risk trades. The same goes for very small accounts. You can’t really trade these undefined risk strategies in very small accounts as you just won’t have enough buying power. Therefore, you have to trade the defined risk counterpart strategies if you want to trade options.

Option Greeks

Furthermore, the Greeks are something to look at. They measure price changes in the option’s price for different scenarios. The Greeks can be quite different for undefined and defined risk strategies. For example, Theta or time decay is much greater for undefined risk strategies. This means undefined risk strategies profit more from time passing by.

Options lose some of their value over time. Therefore, you can sell options and buy them back for less due to the passing of time. But a call credit spread also has a long option which loses some of its value every day. Therefore, this strategy gains much less value every day than a naked short call.

Another Greek is Vega. Vega measures the change in the option’s price for a 1% change in implied volatility. This is negative for short option strategies as these profit from a drop in implied volatility. Here undefined risk strategies profit a little more from a drop than defined risk strategies.

The two images above show Delta and Theta values for our short call and the call credit spread. They are quite different. A Theta of 0.682 means that the credit spread will gain $0.682 for the passage of one day. This value is substantially greater for the short call. Therefore, the short call gains more than five times more than the credit spread ($3.927). These values change over time so that both positions gain even more value every day.

Management – Rolling

Last but not least, there is a big difference in rolling these defined and undefined risk strategies. A common management technique for losing undefined risk strategies (e.g. strangle or naked put/call) is to roll them out to another expiration date. (Rolling is when you close the current position and open the exact same on a later expiration date). By rolling these positions, you give yourself more time to be right, collect further credit and thereby reduce the overall risk. This can’t really be done for most defined risk trades as you won’t collect enough credit. Therefore, an important management opportunity isn’t available for defined risk strategies.

Pros and Cons…

To sum things up, I will sort the above factors into pros and cons.

Defined Risk Pros:

- Limited Risk

- Better ROC

- Available in all Account Types

Defined Risk Cons:

- Less Premium/Lower Max Profit

- Lower Probability of Profit

- Greeks

- Fewer Management Options

Undefined Risk Pros:

- More Premium/Greater Max Profit

- Higher Probability of Profit

- Greeks

- More Management Options

Undefined Risk Cons:

- Unlimited Risk

- Worse ROC (Capital Intensive)

- Account Type Restrictions

Conclusion

It can be quite hard to choose one of the strategy types. Both defined and undefined risk strategies have their pros and cons. Even after weighing out the different advantages and disadvantages, there isn’t a clear winner. In my opinion, it comes down to personal preferences. It depends on one’s personal risk profile, capital size and more.

A good idea is to do a little of both. No one says that you have to pick one of these strategy types. Try both and if one works better for you, stick to it.

There is also a possibility to take advantage of some pros of both the defined risk and undefined risk strategies. I will explain it with an example call credit spread. But again, this can also be applied to most other short defined risk strategies like put credit spreads, iron condors…

The further you move the long call OTM on a call credit spread, the more it will act like a short naked call. If you create a 10+ point call credit spread, it will slowly act very similar to a naked short call. But it will still have defined risk and require much less buying power. Furthermore, the long call will cost much less as it is so far OTM and therefore, the max profit/premium will be quite high.

So just move the long options further OTM to create a defined risk trade that acts similar to an undefined risk trade.

Here is a brief list of the defined risk counterparts for certain undefined risk strategies:

- Short Put → Put Credit Spread

- Short Call → Call Credit Spread

- Short Strangle → Short Iron Condor

- Short Straddle → Iron Butterfly

Here is an infographic recapping some of the key takeaways from this comparison:

(If you want to use this infographic, go ahead. Just make sure to link back to this article.)

I truly hope you enjoyed this article and learned a lot. If you enjoyed the article, make sure to share it with some friends and family with similar interest areas.

If you have any questions, feedback or comments, please let me know in the comment section below

Hei,

Thanks for the excellent explanation on the different trading strategies for options. I am interested in investigating options trading myself but find I struggle to get my head around the associated jargon. Is there an easy way to get into options trading with a low investment ? and what are the best platforms for a complete novice to try it (or are we better to stay right away ?)

Hey Tony,

Thanks for the comment. It is possible to start trading options with limited capital. Nevertheless, I really recommend educating yourself before risking any amounts of money. Options trading and trading, in general, comes with a certain learning curve. It is very important to get some education on trading as you otherwise probably won’t become profitable.

A good and beginner friendly platform for options trading is Tastyworks. You can check out my Tastyworks review. But again, make sure to educate yourself before starting to trade with real money.

As for complicated trading jargon, you could check out my free (options) trading glossary. In it, you can look up some of the unknown and complicated trading terminologies that you will come across. You can check it out HERE.

You have really outlined the different types of options trading here in a rather nice manner. People really need to educate themselves on options on all levels and you have given them a great start here. I know it can be daunting at first, but you have simplified it here for people to really understand. How long did it take you to really grasp and understand the options market?

Thanks for sharing your thoughts. I really appreciate it.

Even though I started to get into options trading multiple years ago, I still wouldn’t say that I fully understand everything perfectly. There are still things that I can learn. In my opinion, it doesn’t really matter how ‘advanced’ someone is, everyone can learn more about a certain topic. Especially topics like the markets are so diverse and complex that there always will be new aspects to learn about.